Karoon Energy

Karooning Out of Control. An opportunity following the WhoDat blunder.

Executive Summary

Karoon Energy is a small (~AU$1B) Australian Oil and Gas E&P, fairly new to owning producing assets, has recently expanded its footprint a little faster than it can handle and has been severely punished by the market for doing so.

Getting strung along by LLOG on a very expensive capex campaign on Who Dat, whilst their core Baúna business experiences significant operational issues and downtime. The Who Dat asset has disappointed in its first 12M of ownership, dramatically diluting EPS and destroying FCF, whilst the opposite was promised.

The company needs to focus on equity economics and not simply empire building. The organisation has grown though equity issuance, and not equity growth. Focus on building per share returns.

Company has been uncharacteristically unlucky. The core assets are reasonable.

At ~$1.30, significant opportunity beckons. Market has punished the equity.

Introduction & Background

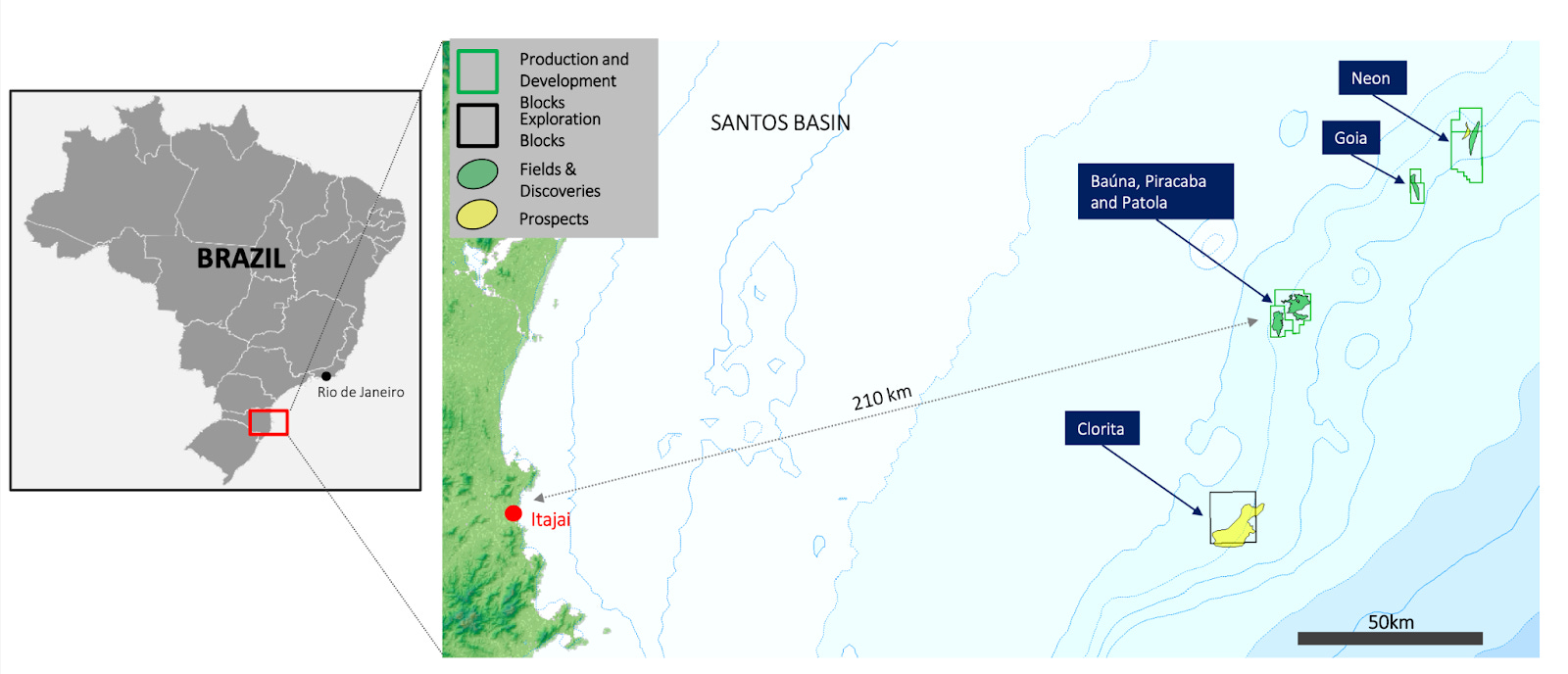

Karoon Energy is an ASX listed E&P company. They own 2 producing fields, Baúna1 in the Santos Basin (Brazil) and Who Dat in the Gulf of Mexico (GOM) (USA)2.

Karoon Energy was historically an ASX listed explorer, however in late 2020 they opportunistically purchased the Baúna field (in Brazil) from Petrobras.

The company was a single asset company for 2 years until the acquisition of the Who Dat field in late 2023.

Baúna has worked out well. The asset was bought at a good time and at a reasonable price. Value was added to the field immediately through successful workovers and 2 new wells, lifting field production from ~15kbd to ~35+ kbd. (The share price moved commensurately). The asset has strong free cash flow, the reservoir & oil quality are very good, the asset quality is high, production rates are reasonable for the size of the investment and the field is declining around ~15%/year.

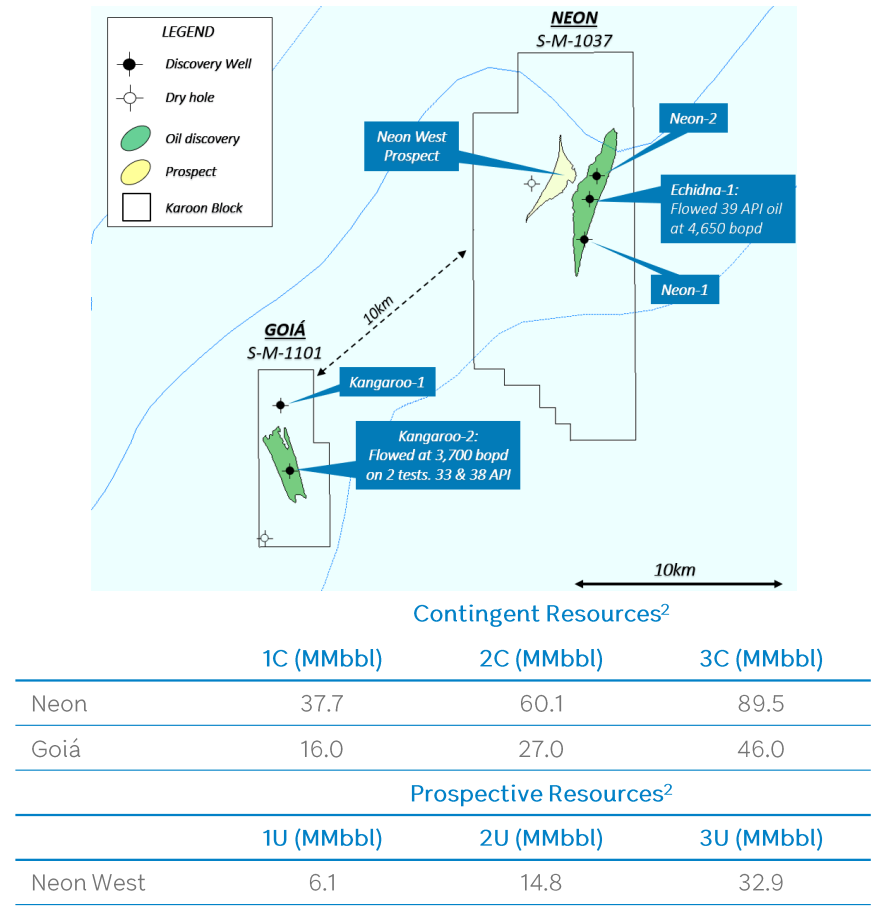

The Baúna field is nearby two other undeveloped Karoon fields, Neon and Goia. These fields have been studied one way or another since 20133.

KAR presented a “Strategic Refresh”4 in 2021 where they reframed the business around also being a hydrocarbon Producer, outlining their new base business (operating Baúna) and their growth opportunities. They are focused on four key aspects:

“Operational Excellence”

Intervention & Patola Development

Neon Area Development

Brazil M&A

Then in late 2023 Karoon surprised the market with a very large M&A deal, purchasing the Who Dat5 field offshore Louisiana (Mississippi Canyon block) in the Gulf of Mexico USA.

Not only had Karoon strongly deviated from its stated M&A direction of specifically looking at mid-life ex-Petrobras assets in Brazil (and Neon/Goia), they moved into a completely new country, jurisdiction and Basin.

Karoon raised a significant amount of debt & equity to finance this acquisition (US$720M debt & equity) to pay for the new GOM field. This cap raise top ticked the share price, which it has never gotten back to.

The equity component of the raise was very large. My initial thoughts were that there was a lot of slack in this newly issued float that the market wasn’t very interested in. Oil Companies equities are not high on the radar of investors, especially small Australian listed producers with a hodgepodge of tier-2 assets.

Karoon also took on significant debt (including issuing a $350M bond) to finance this purchase, levering up the organisation.

Notably, Karoon became a minority partner not only on Who Dat, but also a large component of their asset base. Karoon are now essentially held hostage with a partner who is spending a lot of Capex sustaining and growing Who Dat6. The Who Dat field operator and majority owner LLOG has 2 active drillships, which of course brings opportunity and a large bill7. These ships have contributed two ‘successful’8 near-field discoveries, which the market seemed to have absolutely no interest in.

Problematically, the Who Dat field went offline almost immediately, and has since been plagued with operational issues and has had two hurricane path preventative shutdown related since it showed up on the books.

This capital spend has become the largest issue that Karoon currently faces, on top of adding an asset that was dilutive to EPS. The current amount of capital spend completely changed the company, dramatically changed the return profile of the organisation and has been poorly received by the market9.

Meanwhile, Baúna has also struggled operationally, having significant and serious downtime, both on topsides and downhole.

Administratively, Karoon leadership has been under significant pressure from activist investors10 encouraging the company to reduce capital spending and focus on shareholder returns. This is the general narrative across the largest and most professional oil companies in the world who are firmly focused on providing more return on capital11.

The 2024 Karoon AGM also had some fireworks whereby the Management team had a 26% vote against executive pay levels given the performance of the company12.

The activist case can quite simply be summed up by the following quote:

“Samuel Terry argues if the company changed its strategy, it could pay an annual dividend of 40¢ to 50¢ – equivalent to about a 20 per cent yield at current prices.”13

This pressure continues into 2025, with KAR still heavily investing new capital into Who Dat.

To the board's credit, they have listened and have met some basics such as announcing a small maiden dividend (~4c) and starting a small amount of buybacks.

Looking holistically, given the dual Baúna and Who Dat outages during 2024, it seems we have an organisation that is spread too thin and its focus has been lost and needs to get back to basics.

Sitting here in late 2024, Karoon is in the current State:

Baúna field:

Topsides plagued by Gas compression issues, a major well down due to a blockage,

The entire field just restarted after being offline due to a mooring system failure and emergency situation.

B-88 Well still Offline (~2kbd), awaiting LWIV to correct.

Who Dat Field:

Topsides having Gas Compression issues, with associated downtime.

2 Shutdowns due to hurricane path proximity.

2 Recent nearfield discoveries.

New drill well (WDS) expected to spud shortly in 2025-Q1

Extremely high spending at Who Dat, where KAR are not in control.

Neon/Goia:

Continuing to appraise the fields, and managing significant subsurface risk.

Management:

4 production downgrades in 2024.

Under pressure from local Activists owning a significant chunk of the company.

Market:

The question remains: how much worse can it get?

The following sections discuss the current opportunity present, a brief analysis of their fields, a brief financial analysis, some conclusions and some recommendations for the organisation.

Asset Analysis

I am looking at Karoon by breaking it down into its constituent assets. This is of course from the outside looking in. I’m fairly new to the name and have only been following the company since 2023.

I leave any analysis of the wider macro or oil price environment to the reader. My analysis considers a neutral oil price at its current level (Brent at ca $72).

Neon / Goiá

The current organisation makes more sense after first looking at the Neon and Goiá fields. These are both discoveries from the earlier explorer days of Karoon, well before Baúna arrived on the scene.

Neon was discovered by Karoon in 2015, appraised further in early 2023 and has had a total of 3 well drilled to date17. The field resource size is: 1C of 30 MMbbl and 2C of 55 MMbbl in 2018, increased slightly in 2023 to 1C of 38 MMbbl and 2C of 60 MMbbl18.

Goiá was discovered in 2013 and has had 2 wells drilled to date19. 2C Contingent Resource of 27 MMbbl booked in 2018.

Without delving too far into resources/reserves, the upside scenario at both fields are roughly comparable to the existing Baúna field with ~55 MMbbl 2P Proved+Probable. Whilst this comparison seems appealing, it is too optimistic. The size of the prize is reasonable, but significant geological concerns exist. Discussions of the field continually reference subsurface risk (geological containment/extent presumably). There is very little information available to the exploration geologists, and the geological size of the fields is not large.

Secondly, for this development to be successful with ‘borderline economics’20 it requires:

Geological and operational success in upside scenario at Goiá

Geological and operational success in upside scenario at Neon

Large Capital outlay, Presumably ~US$1B for field development and other ~US$1B for some sort of cut price FPU21

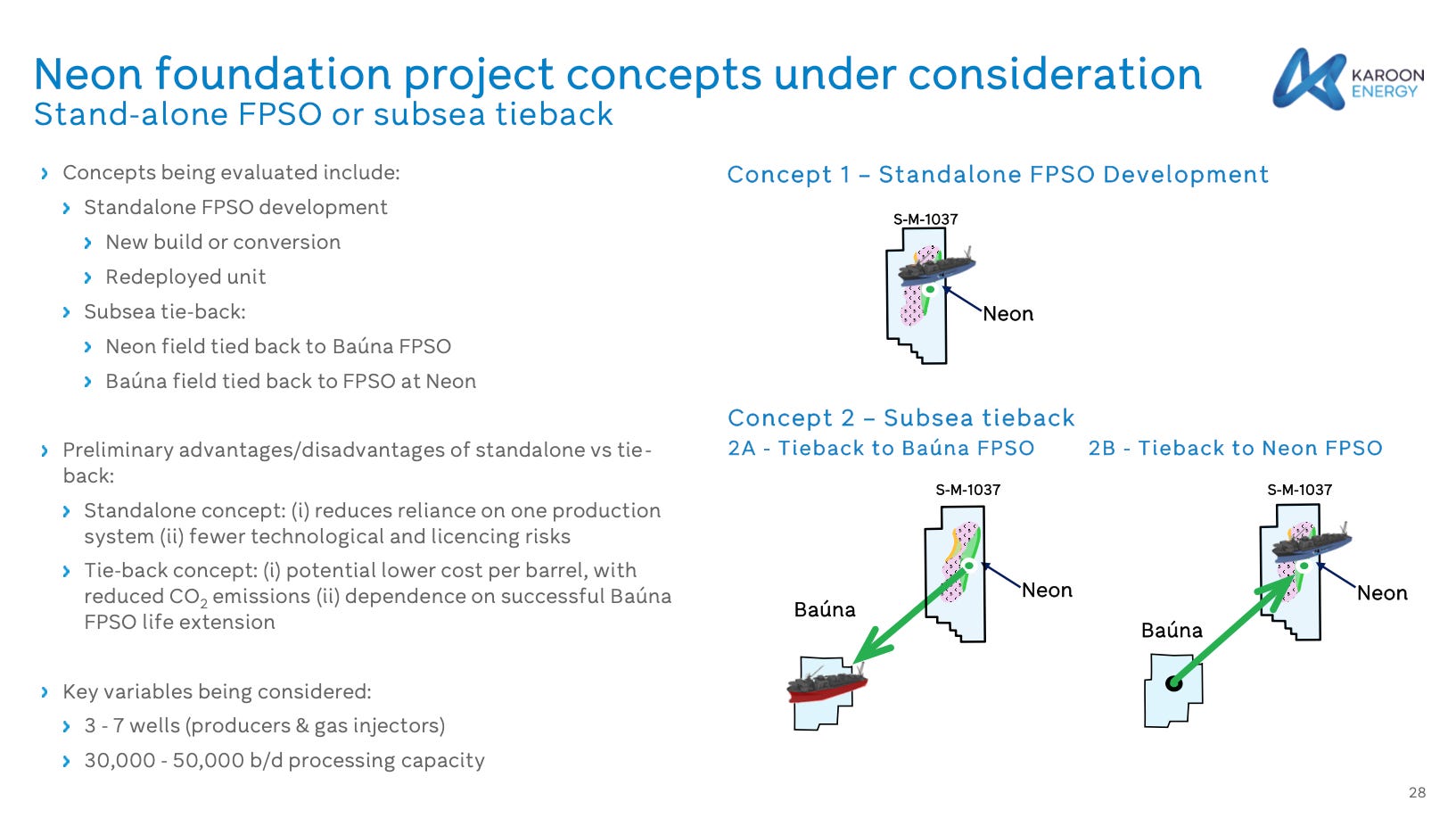

Further, developing these fields would be extremely expensive22 as it would almost certainly require another FPSO/FPU for these fields. The distance from Goiá to Baúna is 50km and the distance from Neon to Goiá is 10km. This distance back to Baúna is likely too long for a subsea tieback and would push the technical/operational limits of the local oilfield.

Usefully (and hilariously) on a recent Neon/Goiá area slide23, Karoon state they have “Strict capital discipline for investments - minimum mid-teens IRR", suggesting a hurdle rate of 16%. With a cost of capital of easily 10%, a 6% margin for development risk is tiny and not worthwhile.

The company flatly states that Neon/Goiá is a “...robust project at 2C level, but sub-commercial at current 1C Resource”, meaning a disastrous outcome in a non-ideal situation, in an endeavour with low base rate success rates.

Lastly, the company has very little field development experience. Every single producing well this company owns has been discovered and developed by other parties. KAR have purely just been the financier and custodian, raising capital, running into purchases and continuing existing drilling plans24.

The maximum operational extent Karoon has undertaken is the management of a drillship adding 2 new wells to Baúna via a tieback and a new flowline into the FPSO. These are standard greenfield subsea operations and routinely performed by consultants or new hires. This is a world away from developing a new field.

Neon/Goiá are best thought of as long term pet projects. The resources are not large, but not nothing. They have been discussed and part of Karoon for nearly 10 years. The 2016-2020 Baúna acquisition idea was presumably highly influenced by the proximity to Neon/Goiá.

The assets surely do not stack up to the board, especially in late 2024 with a lot of other issues. I understand the need to string along the market and local regulator to maintain the sunk cost into the field and to maintain the leases, but the Neon/Goiá endeavour should be put on pause25. The market takes this development like it's going ahead and has priced the capital destruction into the share price26.

Put simply: the Neon/Goiá fields should be re-looked at if/when Karoon is a much larger company, where it doesn’t need to risk a significant proportion of their market cap to develop a legacy discovery. More effort should be put into the communication around deferring these fields to avoid investors interpreting this as another CAPEX black hole.

There is potential here, but the spending at Neon/Goiá must be evaluated vs other available options. There is a hypothetical long term potential that Neon/Goiá inherit the Baúna FPSO following the end of the Baúna fields life, however the timing here is unlikely to line up.

Baúna Field

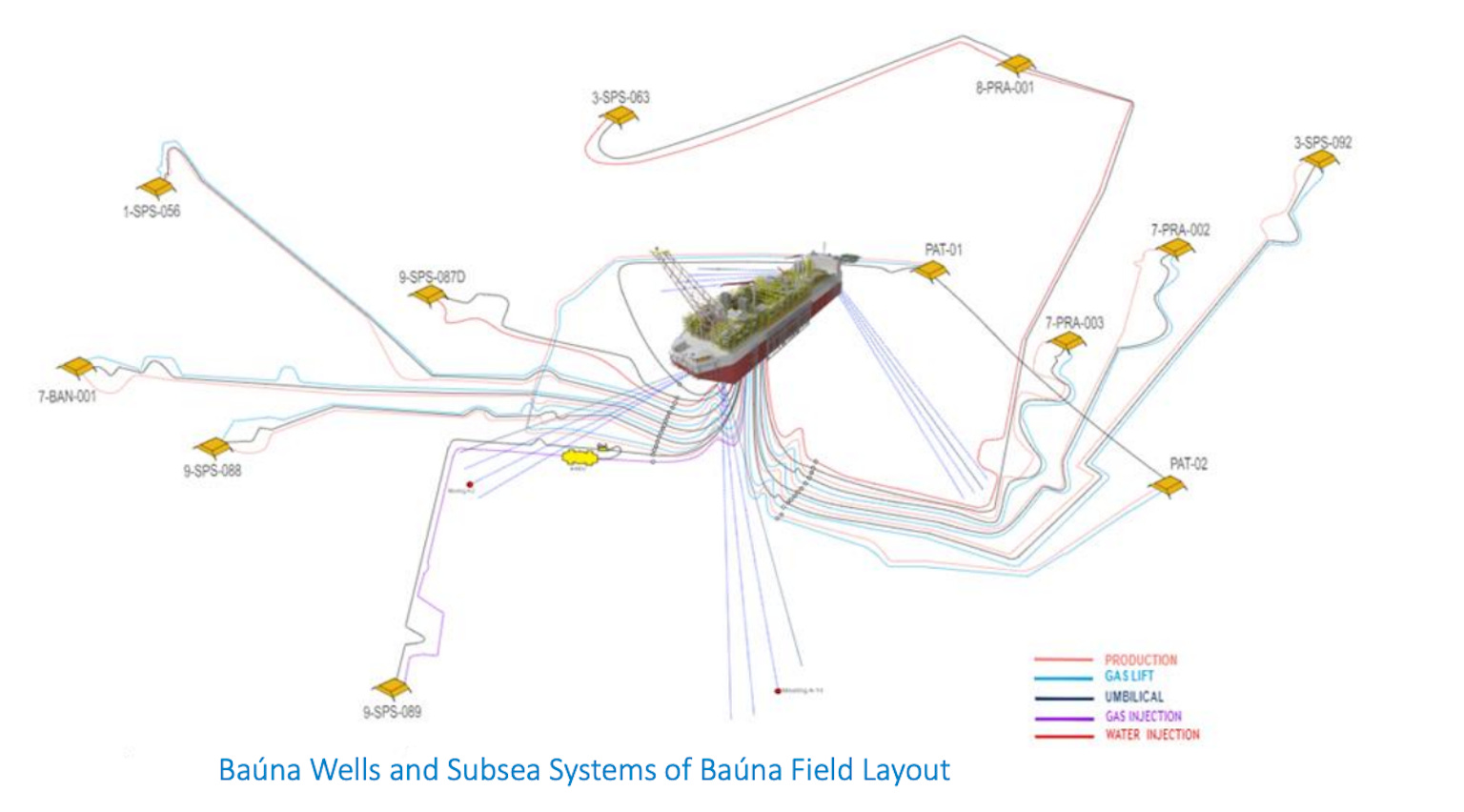

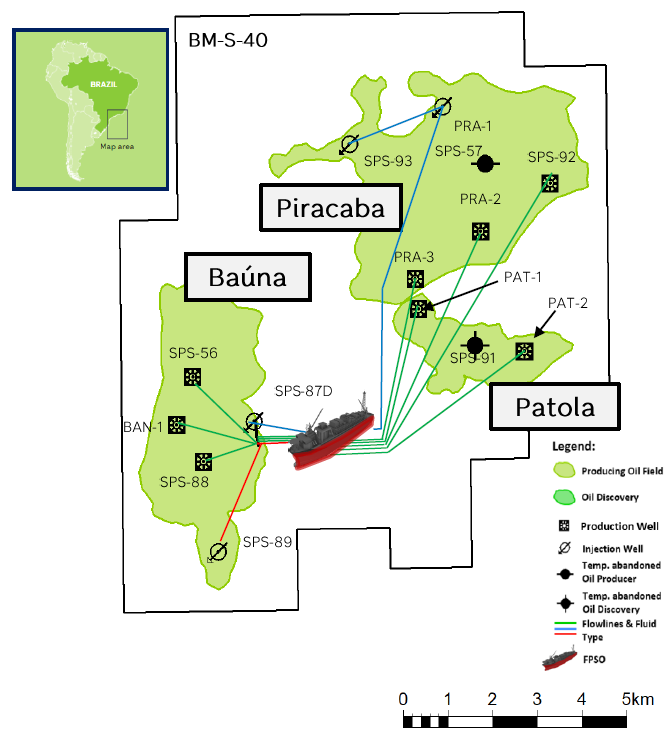

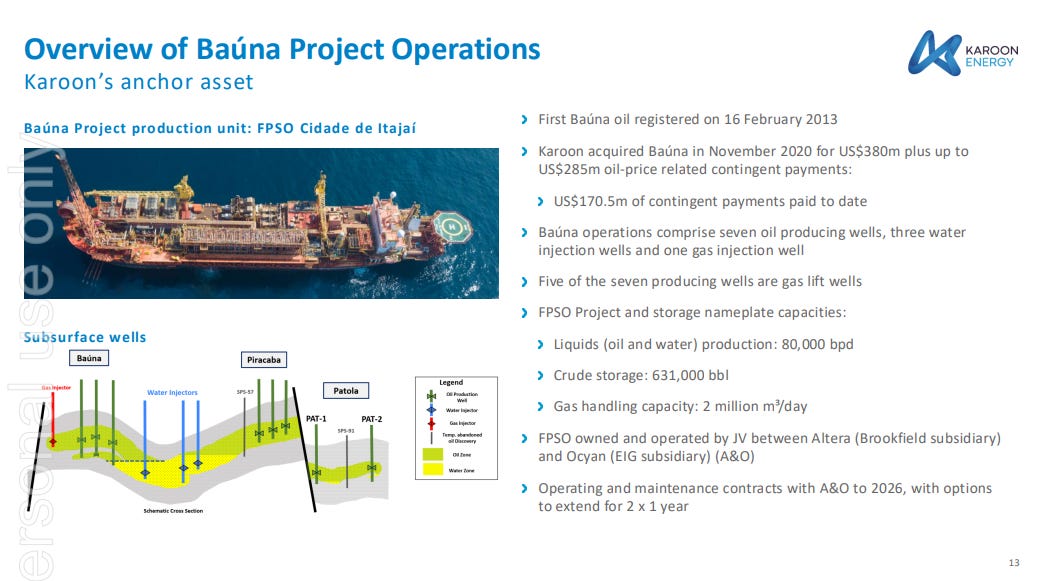

The Baúna field is in the Brazilian Santos basin, block BM-S-40 and is 100% owned by Karoon. It is a conventional oil field 210 km from the mainland, in water depth of 275m27 with good oil quality28 and reservoir quality. Petrobras discovered the Baúna and Piracaba fields in 2008 and put it into production in 2013. Production plateau was 70 kbod. This is the core asset of the organisation.

All wells are subsea, tied back to an FPSO29 named Cidade de Itajaí. There are 8 Oil Producers, 2 Water Injectors and 1 Gas Injector.

Publicised negotiations with Petrobras go back as early as 2016 as part of a large Petrobras multi asset sale to reduce debt. This was later cancelled in March 2017. In 2019 the field was re-tendered and Karoon signed the binding offer. The transaction was completed in late 2020.

Geology/Reservoir

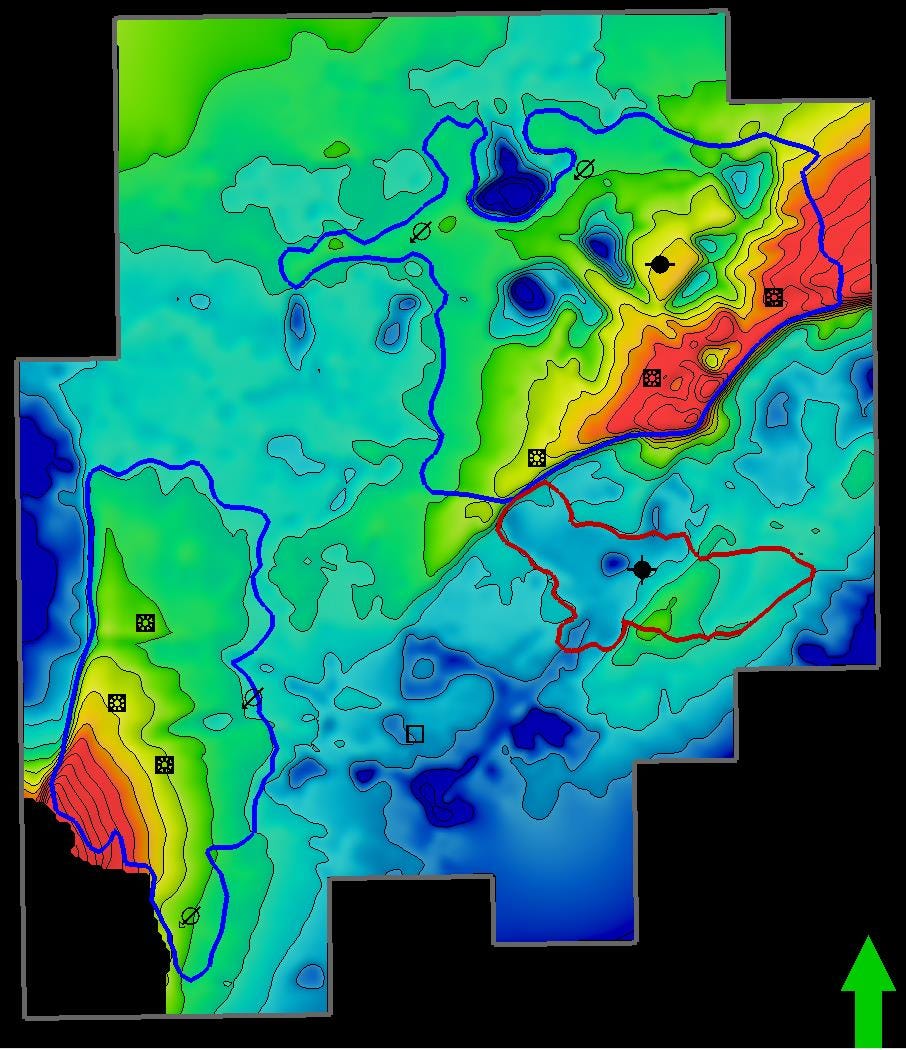

The Baúna area consists of 3 oil charged Oligocene turbidite sandstone reservoirs, Baúna, Piracaba and Patola. There is a strong water drive aquifer. Baúna and Piracaba are regional stratigraphic traps. A strong fault separates the Piracaba and Patola reservoirs.

The reservoir quality is extremely high. The available petrophysics data released discusses 30% porosity, 2-6 Darcy permeability, and horizontally homogeneous sands that are 10-40m above water contacts at depths around 2000m TVDmSS.30 Reservoir Drive mechanism is a water drive. These are ideal parameters, able to sustain very good economics and are generally analogous to prolific parts of the North Sea.

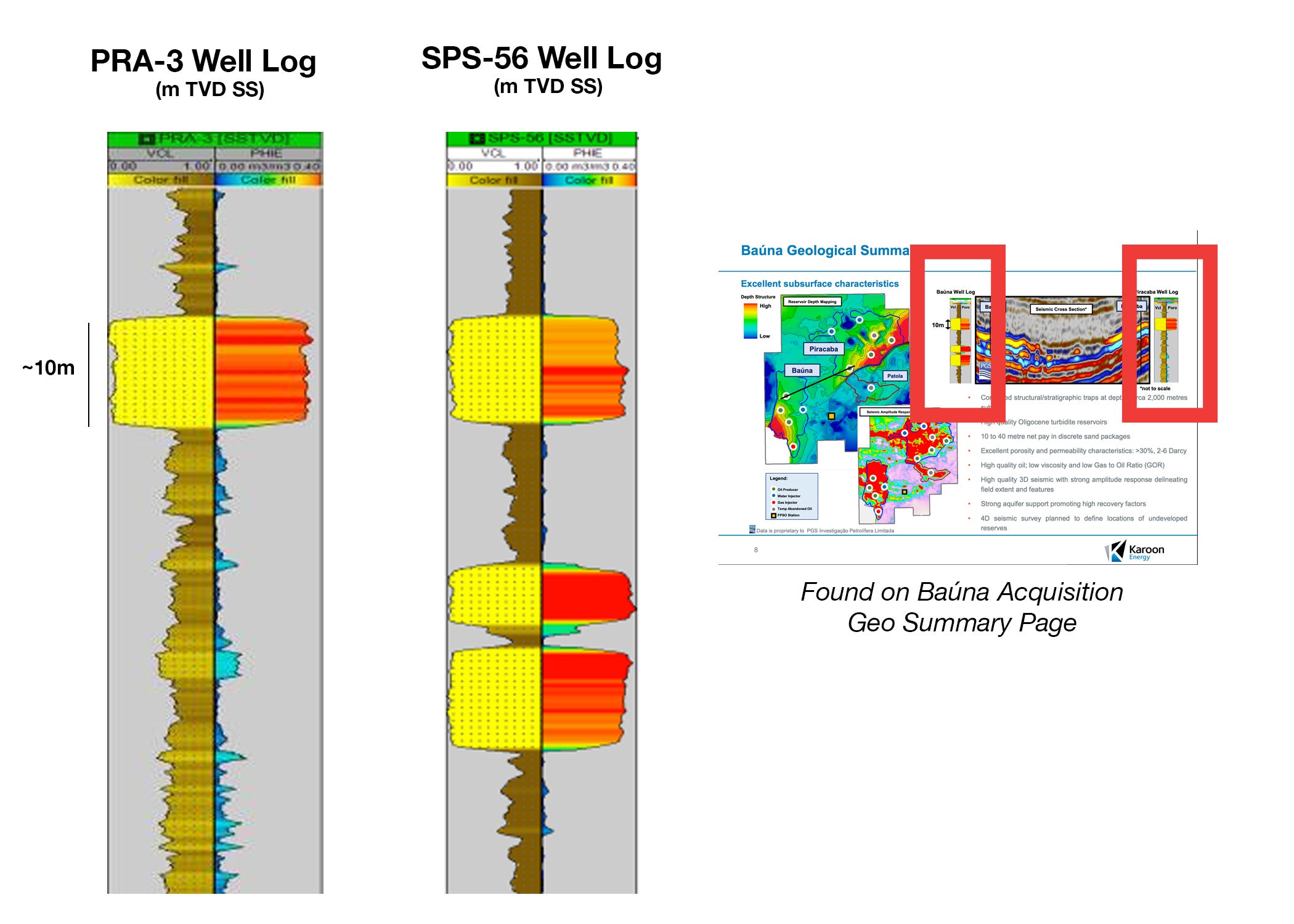

Looking at available well logs, the quality of the sands is unquestionably very high. We have two logs from an early Baúna presentation whereby multiple large 10m+ TVD sand packages are evident across the Baúna and Piracaba reservoirs. These logs are beautiful.

On the micro level, this is about the best quality sandstone reservoir you can hope for, especially in combination with a strong water drive. About the only step up from here is a Saudi Style vuggy carbonate.

The sand quality alone alone does not determine much, the reservoir sands still needs to be large, the standoff from the water contact needs to be significant and you have to drill it correctly. These sands have extremely high potential for spectacularly economic drill wells, especially in the long tail of production. I assume this sand quality is representative of the area3132.

Wells

Some information on the well design is available through the disclosures. The well design is presumably similar across the field, and consisting of:

30” Conductor

13-⅜” Surface Casing around 1200m

9-⅝” Production Casing into top reservoir. ~2000m TVDss

5-½” Tubing (assumed, Unknown, but common with 9-⅝”)

Open hole cemented and perforated. No obvious sand control (or issues)

Upper Completions with:

DHSV’s

Artificial Lift: ESPs or Gas lift (some tubing strings originally installed with no artificial lift)

Downhole Gauge

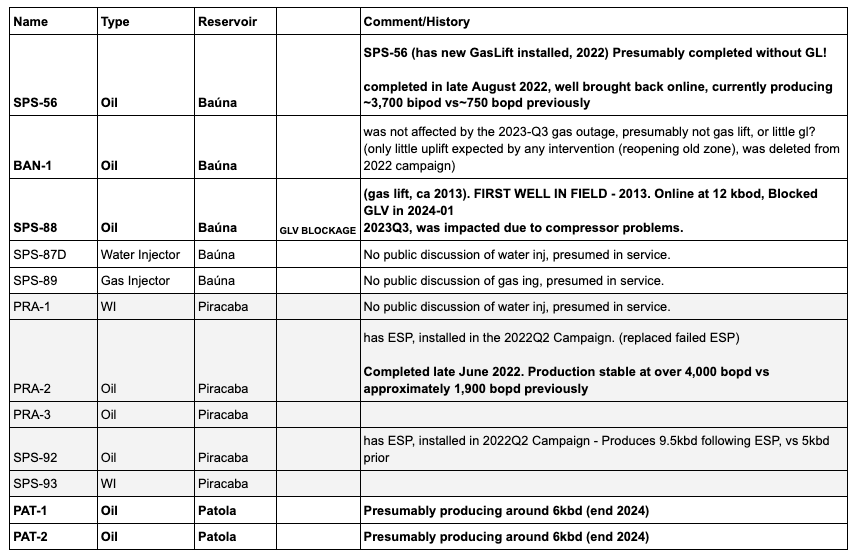

Artificial lift is necessary on this field at current pressures/water cut %’s. Wells without artificial lift no longer flow (SPS-88 shut in due to GLV blockage). This means ESP’s or completions with Gas lIft are critical. This also means gas compression, liquid handing and power supply are also critical.

This logically flows onto topsides water handling capacity. Karoon has seldom mentioned anything along the lines of water handing capacity being maxed out, the only mention is on the startup of the Patola wells in 2023. When Patola production rates moderated, headroom for added water production was made available. This would be an interesting constraint for the operation of the FPSO and we don’t get any info on this. Doesn’t seem like the current limiting factor, but does have implications for any Neon tieback or potential new wells into the FPSO. I would assume the FPSO is processing significant amounts of water, easily over 50 kbwd, perhaps 60 kbwd with a total topside capacity of 80 kbd.

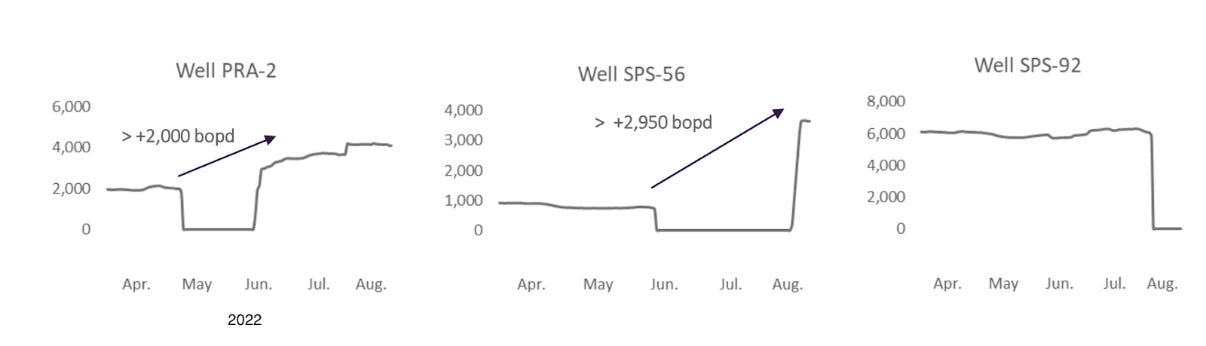

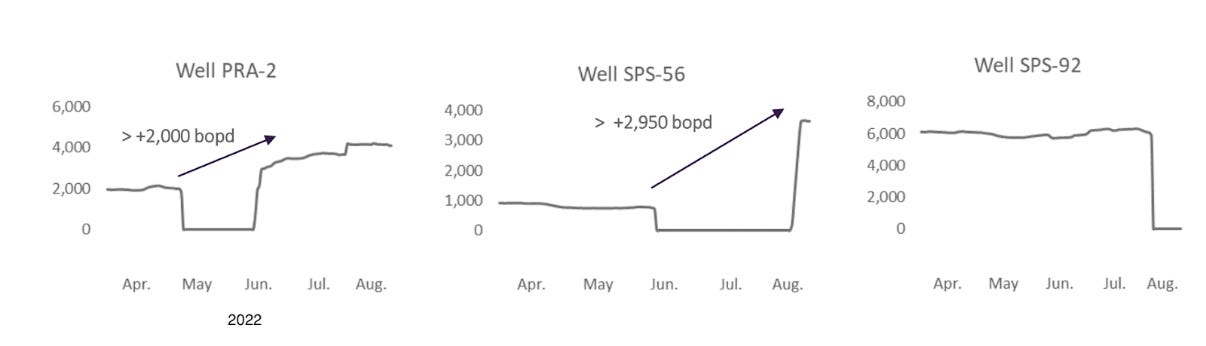

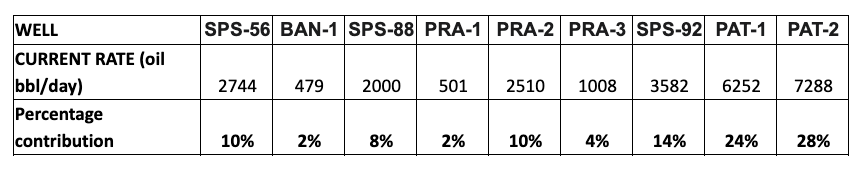

Data for the list of Active wells is as follows. I have collected this from historical ASX disclosures. An interesting element of Karoon is they have been very transparent on much of the Baúna well data.

The Baúna Reservoir Oil Producers33 were the most prolific on field startup, however following the 2022 drilling campaign at Patola, the Patola wells are currently the best producers. There is some history on specific well performance available online, mostly snapshots here and there.

SPS-88 is currently inactive due to the gas lift system not being available. The well needs a ~US$10M LVIV vessel workover to change over the gas lift valve. This is a very common and straight-forward operation with a high chance of success.

It’s expensive as it takes a specialised vessel to access the well securely (remember it is 225m underwater). The actual gas lift valve itself is probably worth ~US$20K. The planned date of this work has drifted from Q4 2024 to “mid 2025”.

Production & Modelling

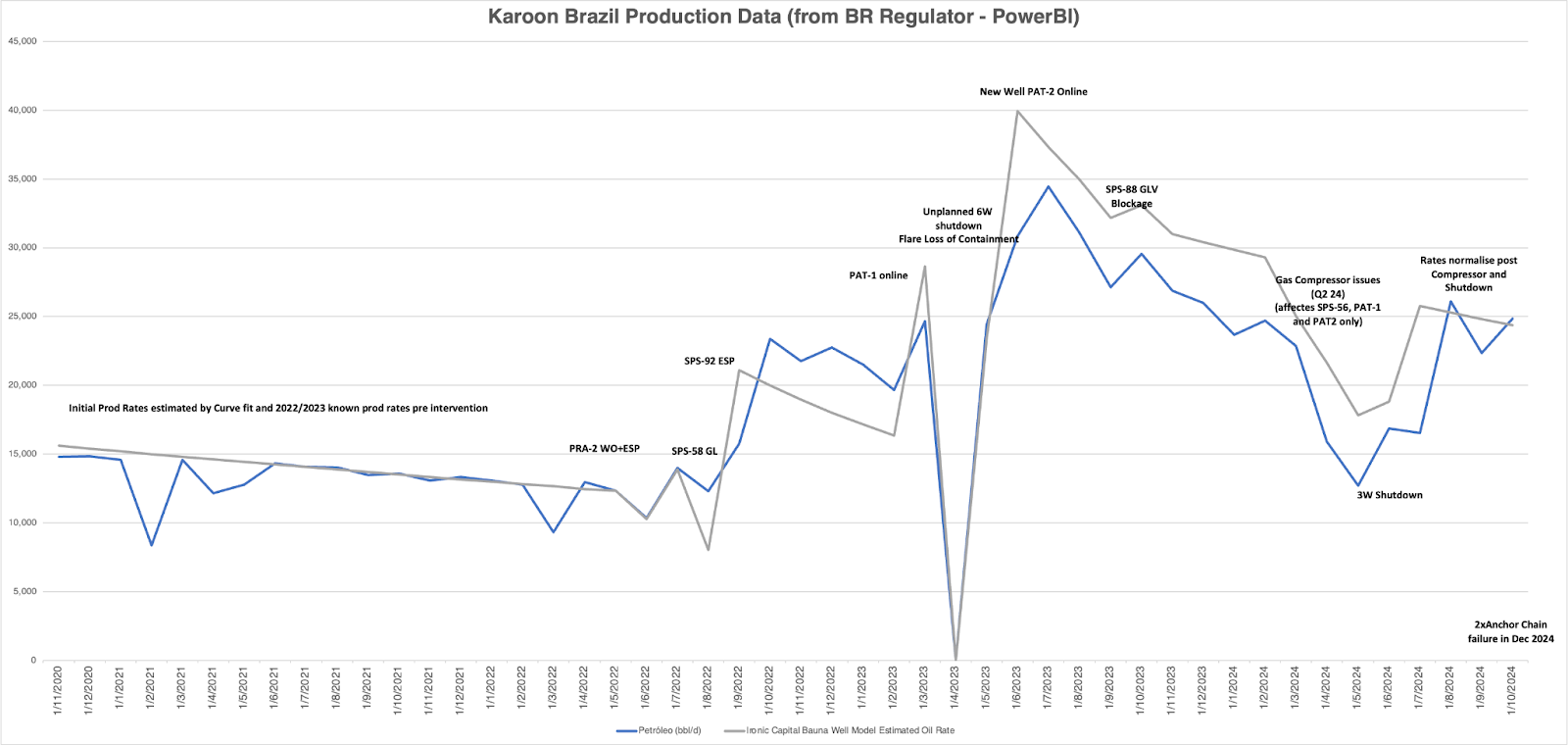

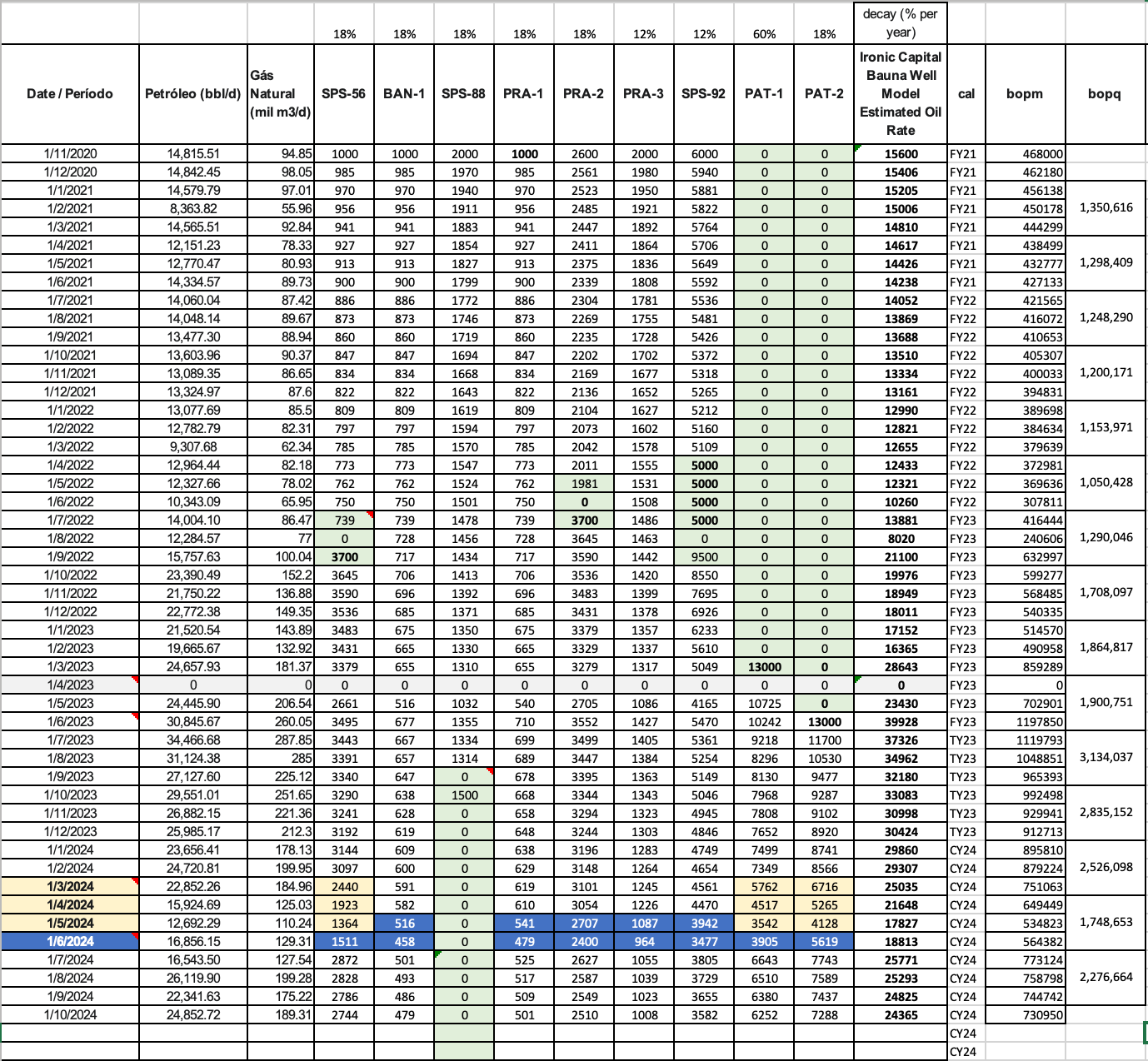

I built a basic Baúna field oil production model to gauge the size of each well and get more of a feel for the field. It showed me the relative importance of the Patola wells but also the old Baúna reservoir wells are still very significant to the platform. I took the Brazilian government oil production data available, graphed it and started curve fitting the known Baúna well data from disclosures.

Fairly quickly I was able to match many key characteristics in their production curve history. The history is dominated by stable decline, a workover campaign in 2022 which bumped production up to ~25kbd, drill wells which bumped the FPSO up to near capacity (40kbd oil, plus associated water from other wells), then a slow decline.

The shape of the averaged production monthly data is a bit spiky, however each spike correlates well to known downtime issues or production improvement.

Assumptions/Inputs:

Assumed 2020-01-01 rates of 2kbd per online well, adjusted later to curve fit and end at known prod rates for workovers.

PAT-1/PAT-2 Drill well initial rates.

Workover data as per below.

Provded Workover Production Rates SPS-88 known blocked in late 2023.

Whole field shutdown in 2024-12-15.

2024-Q3 is 44% higher than 2024-Q2.

Production currently around 25kbd (2024-12).

I modeled Production rates per well as follows:

I don’t have any individual well data prior to Karoon’s ownership so I can not estimate total production per well. However I estimate the 2 Patola wells that are approximately half of the fields production, 5 are reasonable contributors and 2 wells in late life34.

Whilst not immediately useful, this can help gauge the impact of future production events. It's likely the Patola wells need minimal gas lift and have low water cut.

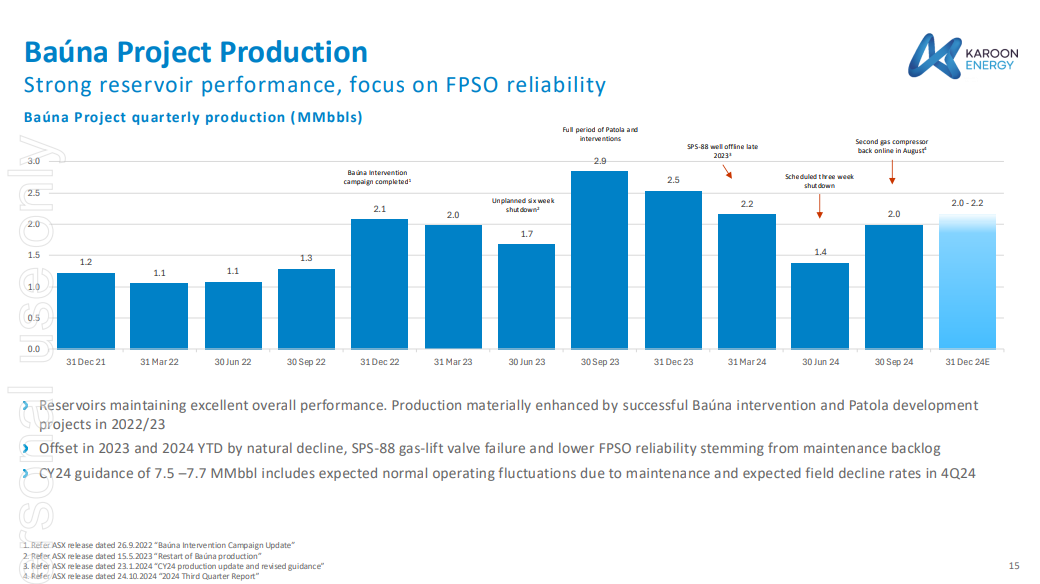

The latest published Production Summary is as per the below:

Baúna Topsides and Downtime

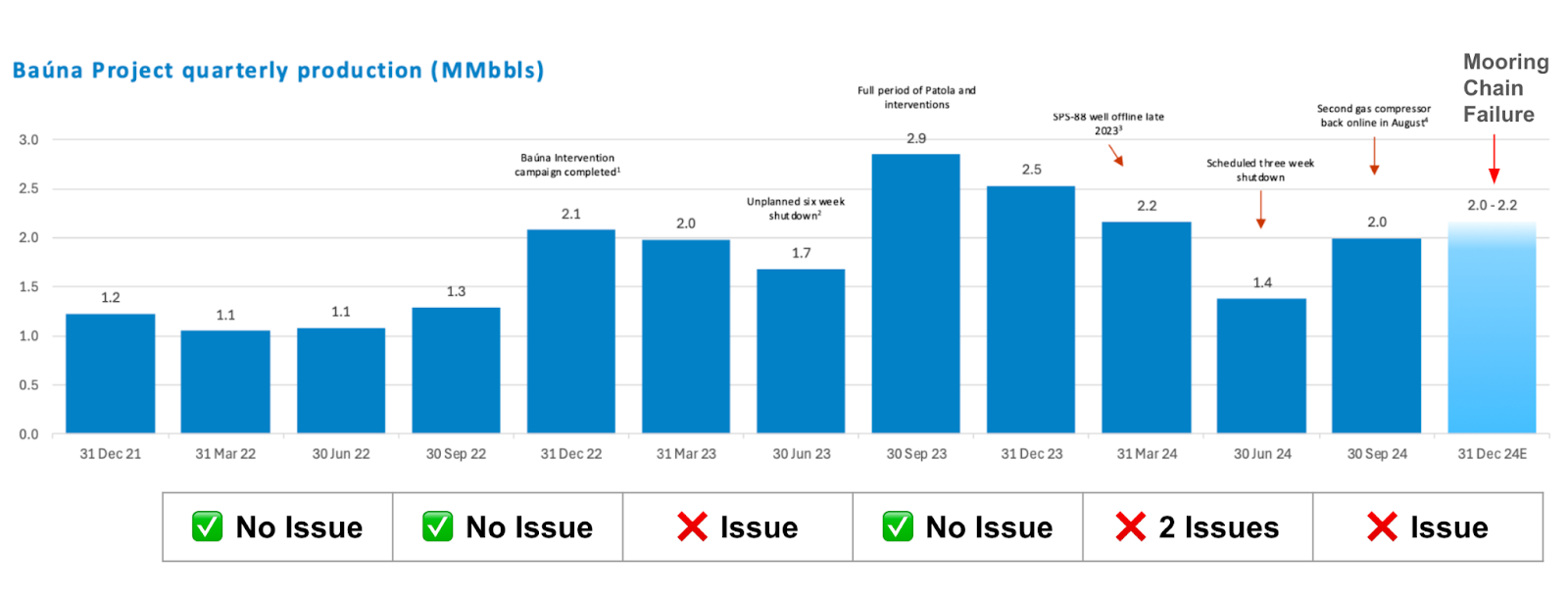

The largest problem with the Baúna field is the uptime of the FPSO, notably the Gas Compression System. There have been many downtime periods within the previous couple years.

The FPSO has had very large outages in both 2023 and 2024, and also whilst I write this the entire field is again offline for unplanned emergency repairs (Mooring chain failure).

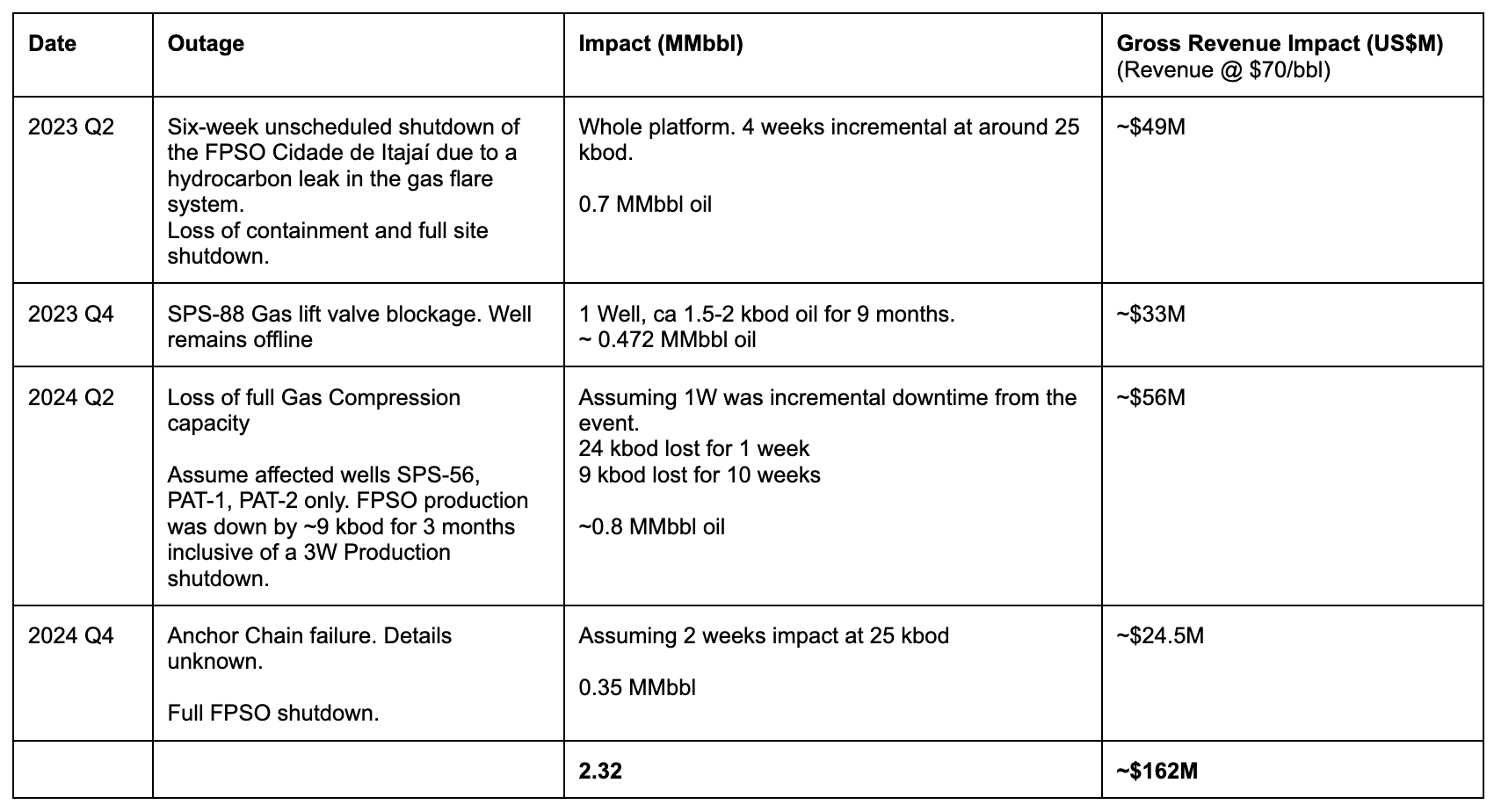

Roughly adding them up from my well model Baúna produced 2.3M less barrels of oil due to unplanned maintenance. This is highly significant and at $70/bbl equates to around US$162M or ~AU$231M.

The FPSO has mostly fixed costs, producing 5 MMbbl oil costs roughly the same as producing 7.3 MMbbl oil.

This downtime is unacceptable by anyone’s measure.

Whilst downtime is part of running an oilfield, this much downtime stands out like a sore thumb. The Baúna FPSO is only around ~12 years old of a presumed 25-30 year design life, the age of the FPSO isn’t an issue, but it seems like the integrity around the gas compression/distribution system and subsea mooring systems are more problematic than they should be. Even more concerning is that the mooring chain failed in summer time, not the heavier waves of winter.

Losing gas compression is operationally critical for mid-late life offshore wells, but this only shuts in wells. Losing an anchor line or two in bad weather can be a death knell for an FPSO. The ship needs to be anchored securely to Safely hold the riser the wells in-situ to produce hydrocarbons through. The Santos Basin wave energy is not as high as the North Sea, where FPSO’s are also built to beam (pivot) around a core (turret) to align with the direction of the harsh weather35.

The general sense I get is that the FPSO has been lacking maintenance. This is not atypical for assets which become part of transactions36.

Why is this occurring?

There is very little detailed disclosure around the gas compressors and especially the problems.

The 2024-10-28 “Brazil Field Trip” presentation is one of the latest presentations on Baúna, and has an added focus on the downtime issue. Worryingly we see this line … “lower FPSO reliability stemming from maintenance backlog”. No more detail is provided.

For a mid-life FPSO this doesn’t seem great, especially given the downtime. Obviously this is now being prioritised. The ship has been in the same position for roughly 12 years in a corrosive environment offshore so integrity issues are part of the deal. But they need to be managed.

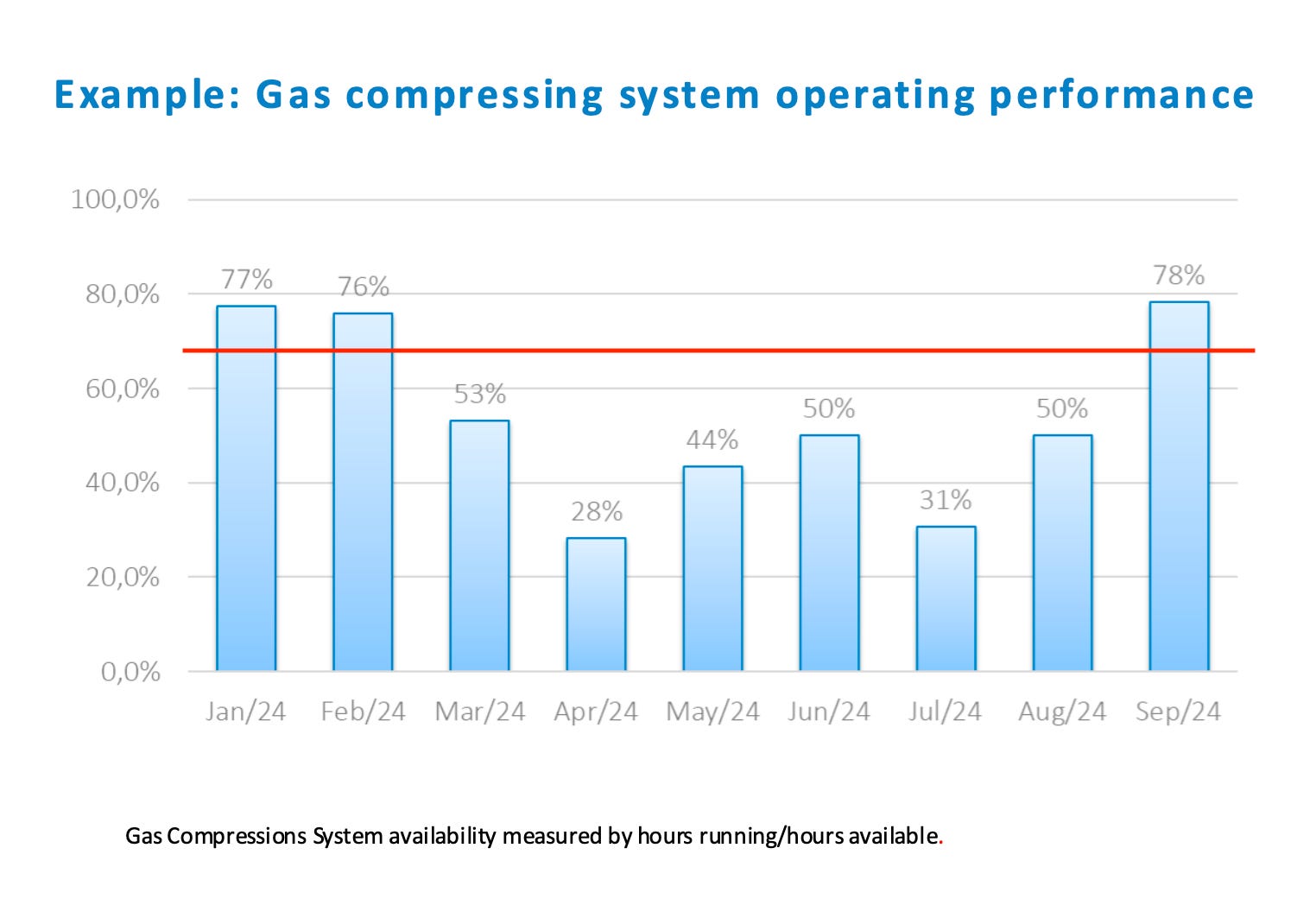

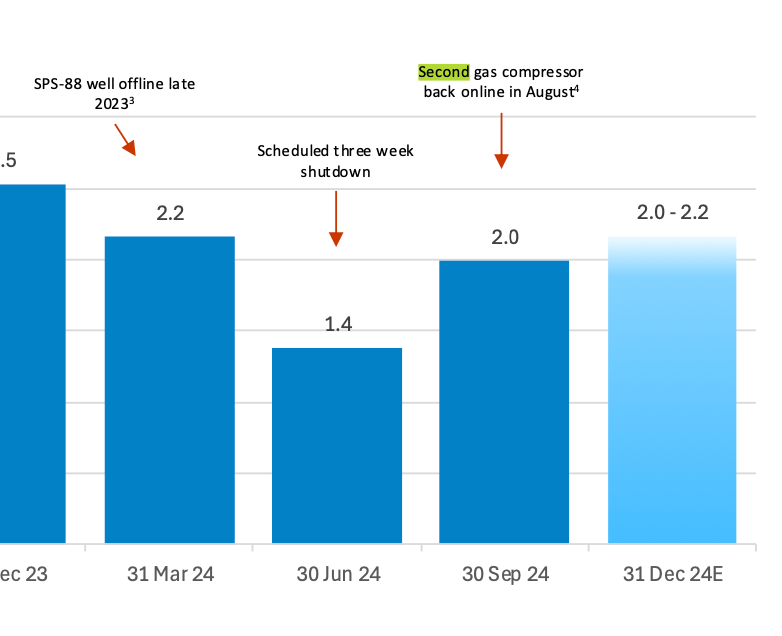

Importantly, the field production is reliant on “2 out of 3” gas compression stations working, which is shown on the below chart does not bode well for optimal production. Seeing this chart is wildly disappointing.

Conversely, there has only been 3 months out of the past 9 where the required amount of gas compression to optimally produce the wells was available. Baúna gas compression is running on the edge. This is with the SPS-88 well offline, which would normally be sucking a lot of the available gas-lift system. This uptime should be better than typical without SPS-88 online.

Recently Karoon have upped their disclosures around the Gas Compression System. I can’t find any discussion on the FPSO’s Gas Compression system pre 2024. It’s a new hot topic.

Karoon has defined “Compressing System Operating Performance [Availability?]”, in terms of hours running on hours available. This seems a little conflated, as I’d use “hours available” as the numerator and total hours as a denominator. Their use of English seems poor too. This work may be translated from its original Brazilian author. Regardless, I will interpret it as an availability measure37.

Karoon has set a goal of 90-95% efficiency, which seems good and needs to be a key focus for the business. To be clear, some downtime should always be acceptable. (If uptime is 100%, the operators may be spending too much).

The good news is gas processing topsides is a common and well known technology. The modules are all above sea level and easily observable. This issue shall pass.

Finally, in the 2024-10-28 “Brazil Field Trip” presentation seems to say “2nd Gas compressor back online in August” on page 15, but on the following page it says September. Tiny discrepancy, but again, details around key disclosures are important. These compressors have cost Karoon hundreds of millions in deferred oil (losses).

Baúna field Acquisition cost

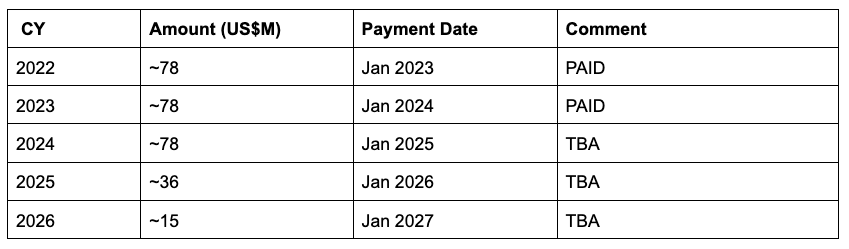

The terms of the Baúna field acquisition was US$380M upfront, with US$285M of contingent payments. The contingent payments are Brent oil price linked, as the contract was negotiated during 2020 with historically low oil prices. I assume the full contingent payment will be incurred38.

Funded with AU$284M Equity Raise and available cash.

The timing of the contingent payments are:

FPSO Cidade de Itajaí

Lets touch briefly on the FPSO costs. These are important to understand the unit economics.

The 2024 Bond issue supplementary data is the best source for looking at the operational/leasing costs.

FPSO Cidade de Itajai disclosed costs are made up of operating costs and the Charter lease costs

The operating contract is with OOG-TKP, an affiliate of Teekay.

This covers crewing the vessel, managing the handling, processing and storage of crude oil, water injection, gas lift, gas export and transferring crude oil to shuttle tankers.

Operating costs are direct operating expenses.

TY23 costs were US$30.2M in 6M, or a day rate of US$165k/day, or approx US$60M/year.

The charter lease is with Altera & Ocyan.

This covers maintenance of the Cidade de Itajaí facility.

Altera & Ocyan are responsible for any replacement costs or costs associated with repairs.

This lease is capitalised.

TY23 capitalised lease D&A costs were US$30.4M, or a day rate of US$167K/day, or approx US$61M/year.

The above day rates are back calculated and assumed to be close enough. Ship contracts are presumably day rate + consumables + indexed.

Baúna Unit Costs

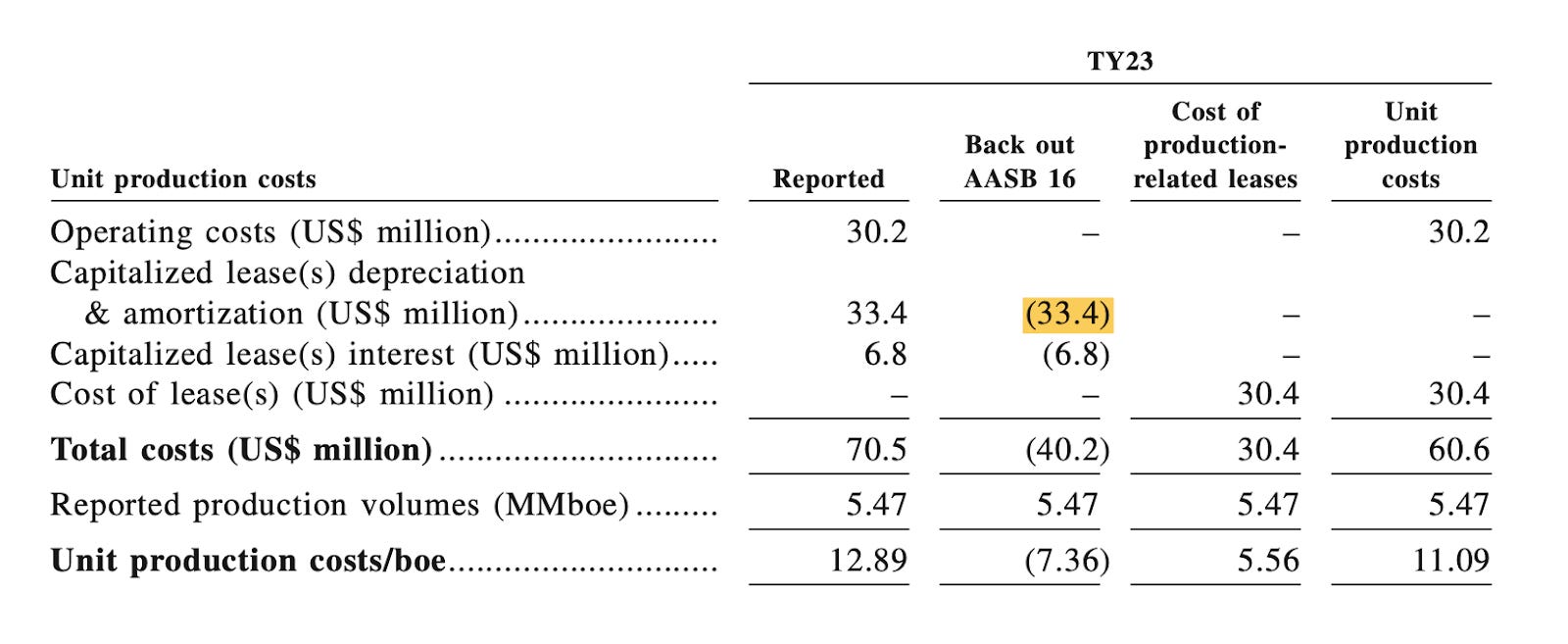

Karoon calculate their Unit production cost in the following way: Dividing the total operating costs, plus the costs associated with the Floating Production, Storage and Offloading (FPSO) facility charter, by the reported production volume.

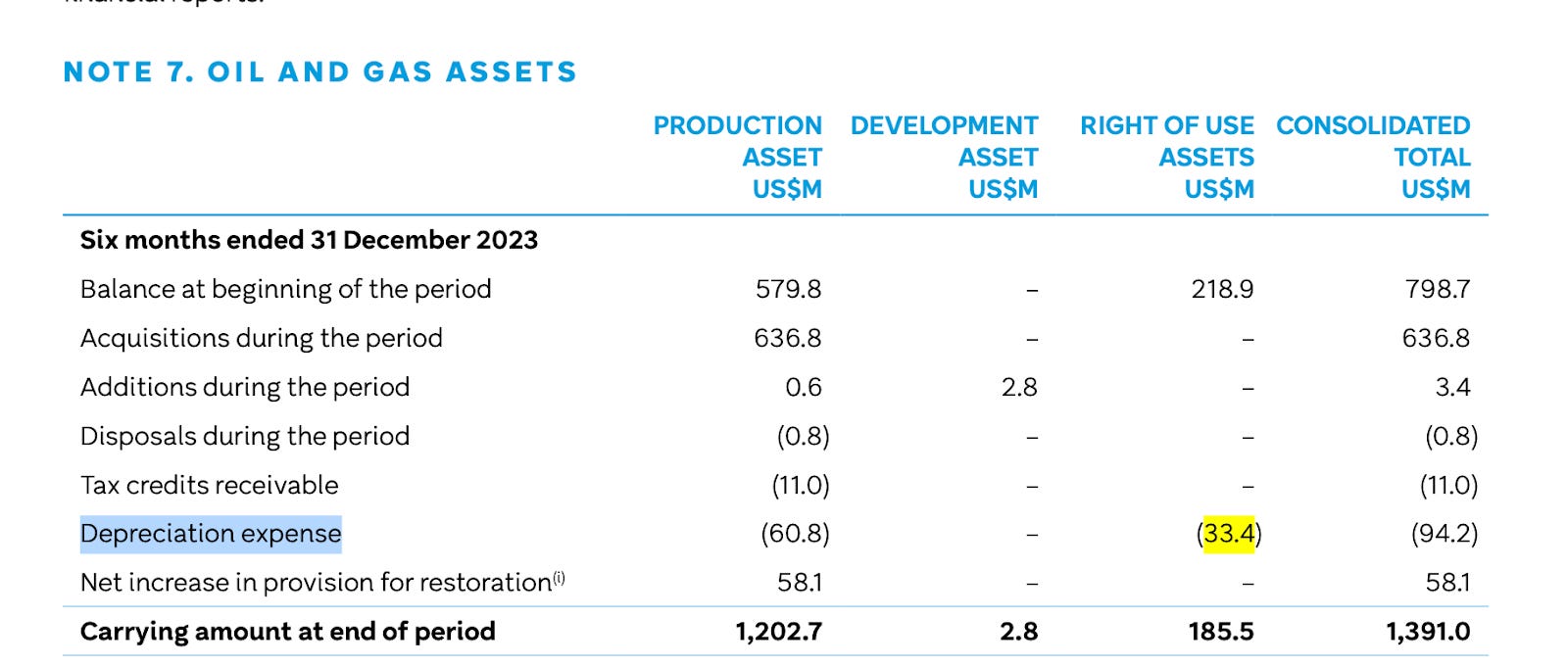

The operating cost component is easy to find, however the costs associated with the charter are not as they are considered CAPEX and depreciated. The bond issue disclosures step through the calculation process (and an adjustment for AASB 1639). Given we know the contracted costs are fairly stable for the FPSO, this assumption will work for future years. Further we can use the depreciation figure for the ‘Right of Use Assets’ (FPSO Charter CAPEX) from the Annual Report, which was -$33.4M for TY23 (6 month period) (matching the bond issue data) and $57.5M for FY23 (12 month period).

The Baúna unit costs can be simplified to be around US$120M divided by the number of produced barrels over a year. The depreciation figures are given halfly, so a unit cost can be calculated accurately each half. The important input is the number of barrels produced (or really how much downtime during the month is incurred and how much decline Baúna experienced).

These unit prices are fine and ballpark for this basin.

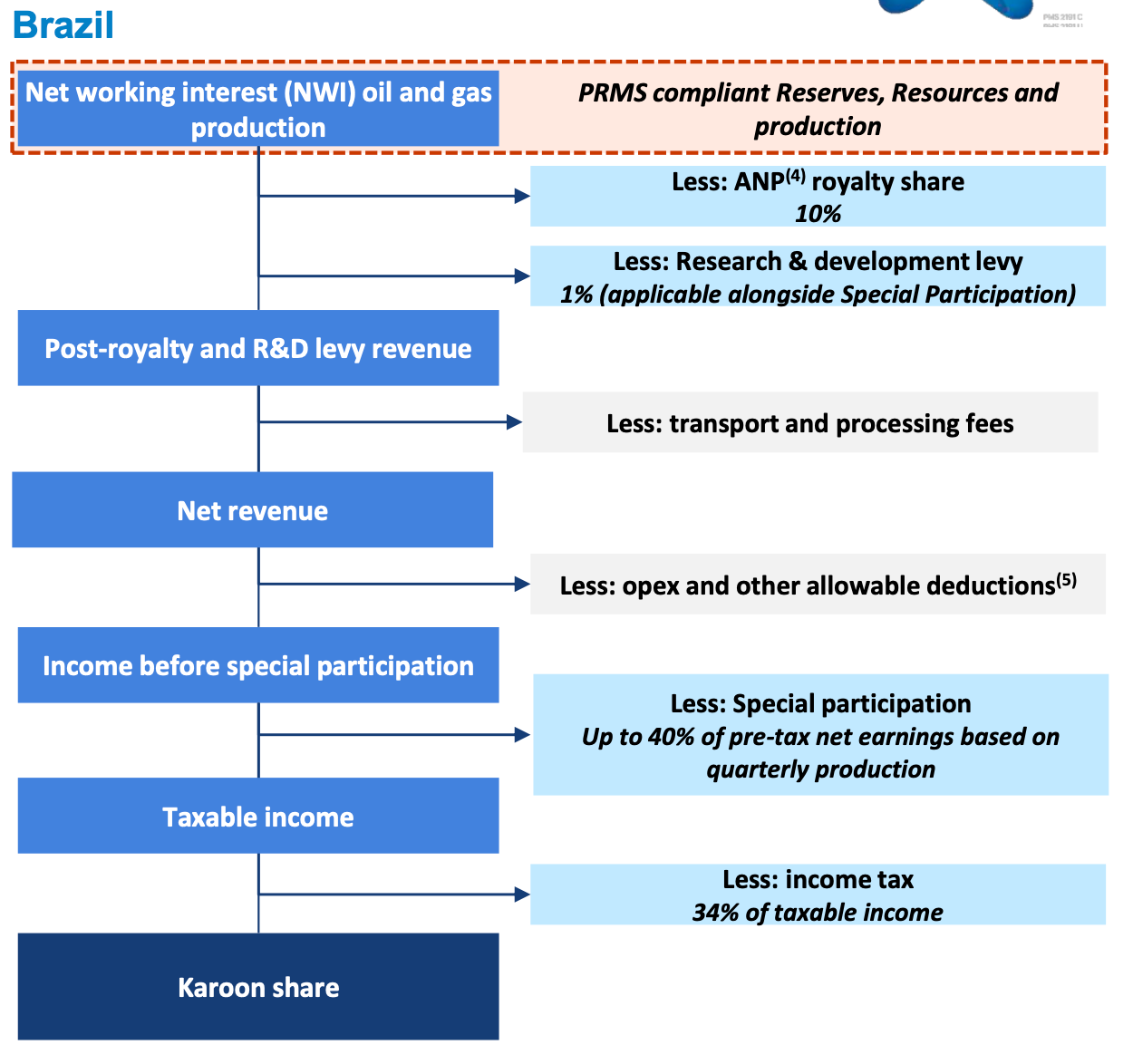

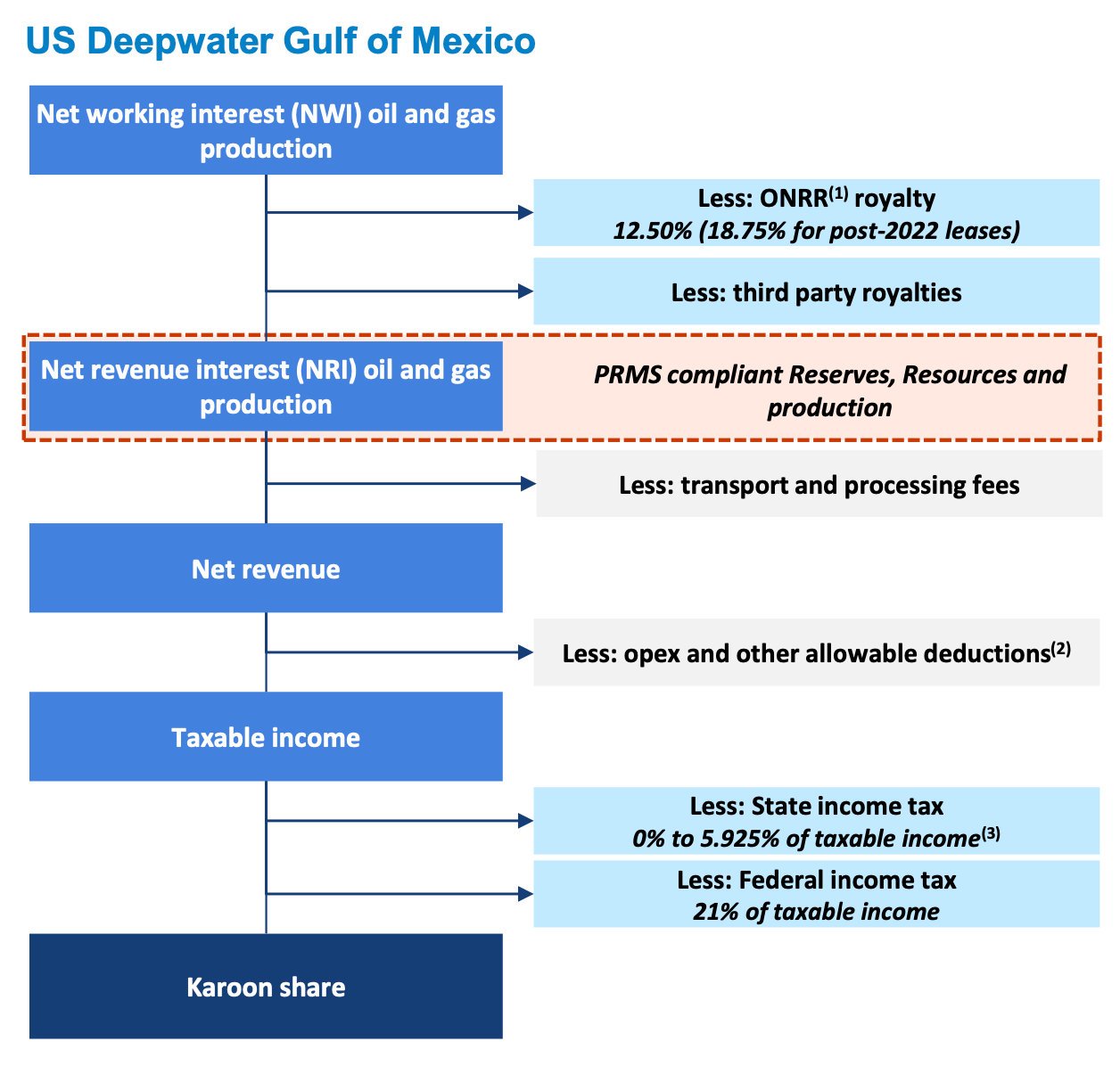

Taxes & Royalties

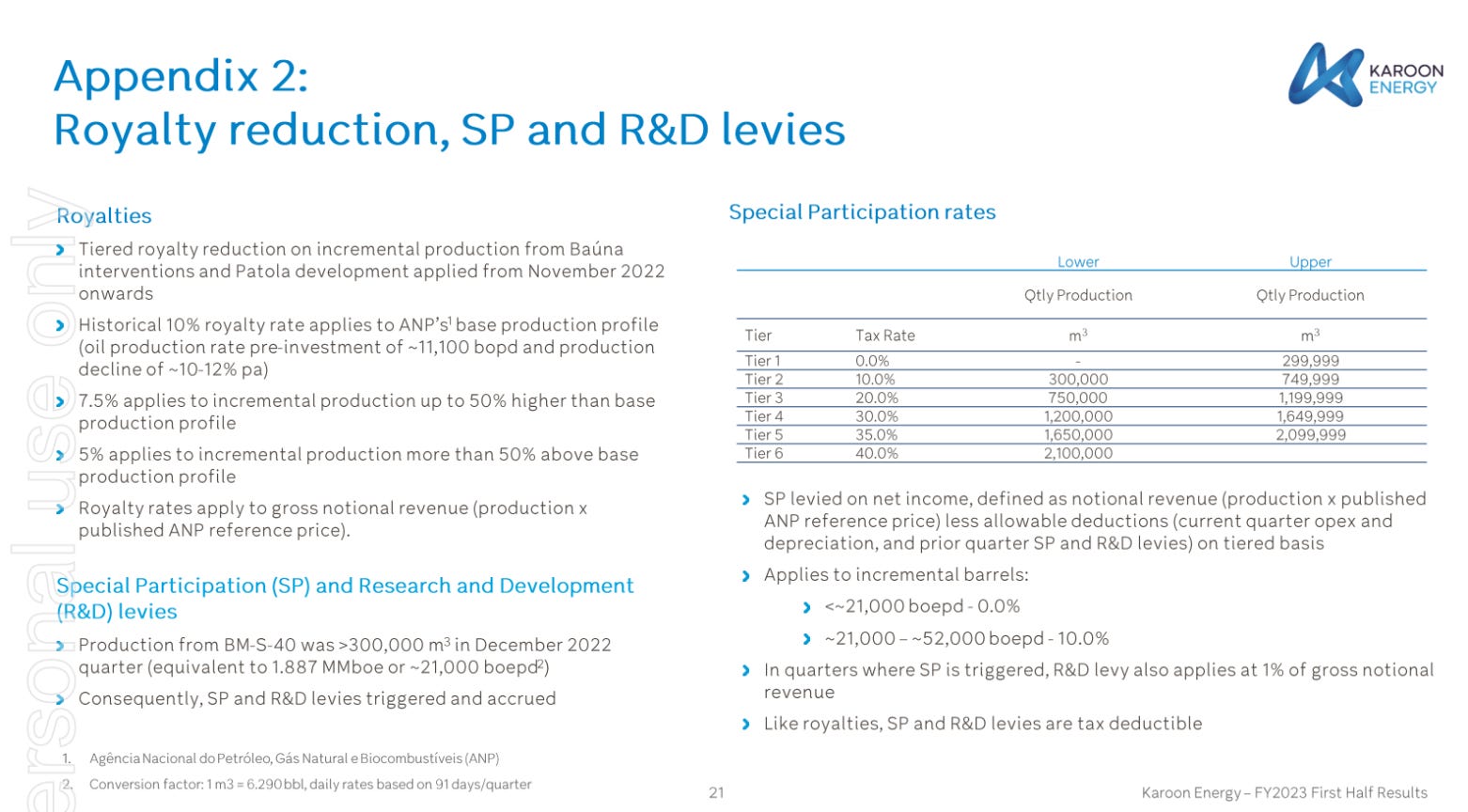

The Brazilian royalty rate is 10% paid on gross production revenues.

In Oct 2022, Karoon negotiated a reduced rate of 7.5% on some of its recent production growth (Patola & Workovers). Production greater than 50% above the original base production profile is rewarded with a 5% royalty. Assuming an ~9.5% royalty rate is appropriate.

There is also a “Special participation tax” (SPT) when quarterly production exceeds 1.9MM bbls (21kbd).

Baúna is in tier 2, giving a 10% SPT rate, this is from the table shown below. This applies only on production above 21kbd40. I.e. in TY23 where ~5.07MMbbl per produced, th

There is also a 1% R&D levy applicable in the quarters where the above SPT is paid.

In TY23, Karoon incurred $8.7M of SPT and $4.3M of R&D Levies on top of the $32M of Royalties, so the SPT+R&D for Baúna is currently around 40% the size of the normal royalty.

With the expected decline rate of Baúna (and patchy uptime), this SPT shouldn’t apply longer than another quarter or two.

Brazilian Corporate tax rate is 34%41.

In 2023 Brazil added a temporary crude oil export tax, which levied a 9.2% tax on all sales volumes (March 1 2023 through June 30, 2023). This tax seems to no longer be in place.

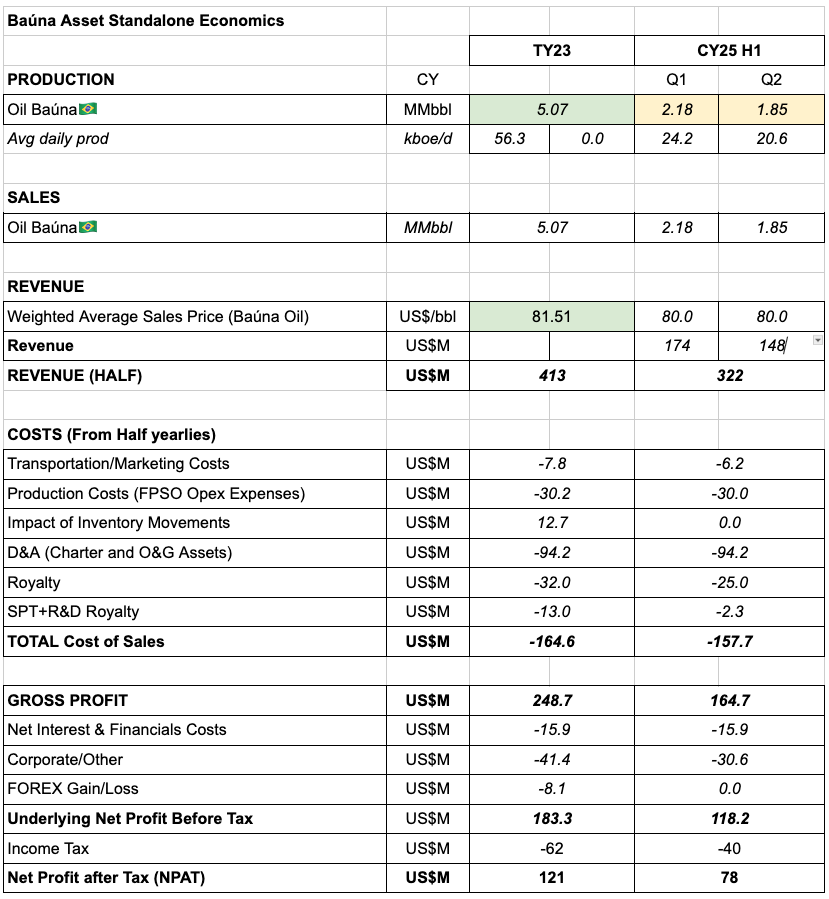

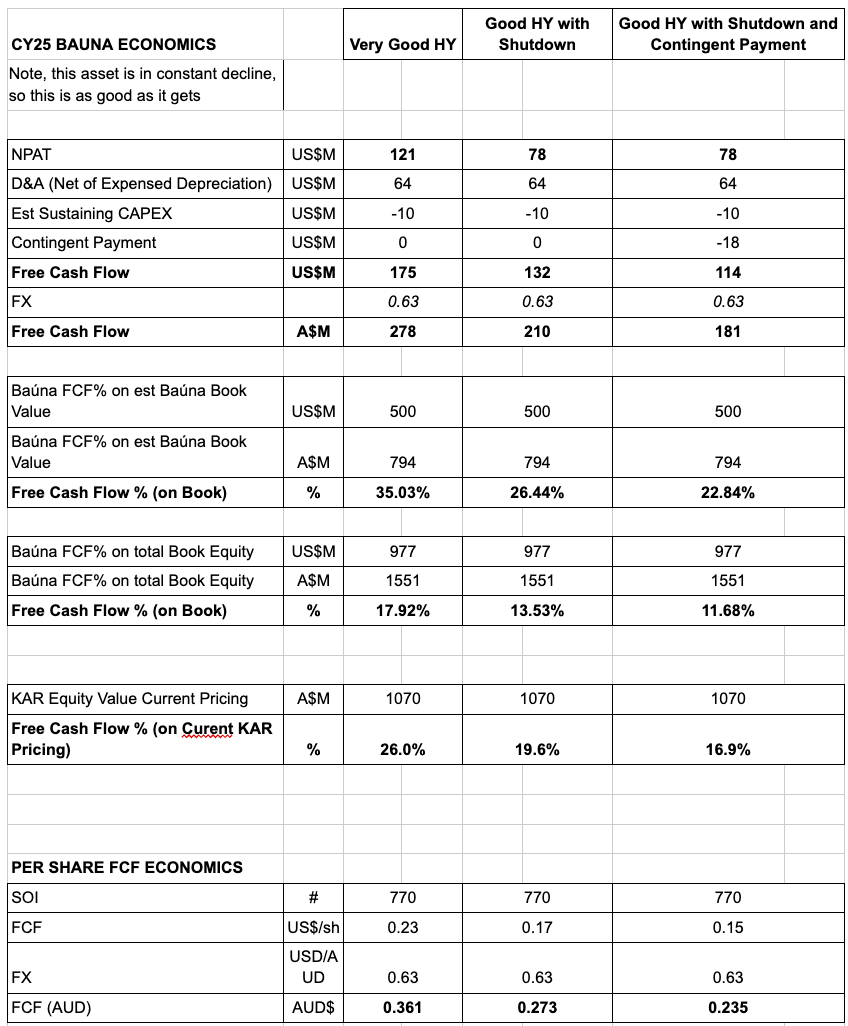

Overall Field Economics for Baúna

Disclaimer: the finances are not my day job (as you could perhaps tell from the detail above).

Below is my attempt at gauging a potential calendar year of earnings from Baúna. Note that the production should decrease each year, so taking this and assigning an earnings multiple is not really valid, but this is somewhat relevant still as only a very small multiple needs to be assigned.

I have focused on FCF unit economics too, as that is what can be paid out. The scenarios I have chosen TY23 for a very good half, CY25 estimates representing an average quarter (with a prod shutdown, without contingency payment) and CY25 with a HY contingency payment included.

NET PROFIT ESTIMATE

FCF ECONOMICS (AND PER SHARE)

Where to from here with Baúna?

The next logical question is where does Baúna go from here? There are a few obvious improvements, but I don’t see any significant issue that isn’t fixable. Having lived working managing assets like these, I do get a sense of a bit of bad luck too. There are obvious maintenance issues but they have had a bad run.

Here is my list of suggested areas of near-term focus

Fix the Baúna Gas Compression issues and associated maintenance backlog.

Improve Maintenance planning.

Fix the mooring chains, examine all mooring chains and system components.

Proactively scour the platform for weaknesses in the gas lift and ESP electrical system.

Execute LWIV Vessel campaign to replace gas lift valve in SPS-88.

Just flow and liquidate the asset.

The workover of the SPS-88 well has been delayed at least three times from its initial planned date in the fourth quarter of 2024 to mid-2025.

Once the Vessel is set up and connected to the well, this is a very standard operation. It should only take a couple days. Unfortunately getting a LWIV is fairly hard and there is likely a need to procure a local vessel and team, limiting LWIV availability. It should restore around 2kbd of production to the platform.

The chance of success for a GLV changeout is in the 80-100% range42.

Managing an asset well enables the ‘luck’ which creates a good half. Just looking at Baúna 2023-2024 they have had an unlucky run. Three out of four halves have been plagued by an issue. There’s a good chance that Baúna simply doesn’t have an operational problem for a 6M period.

There is a low bar here and a low valuation. Upside is very simply achieved by just flowing the asset and having a period without a major downtime event. There is also significant upside available with a slightly higher oil price43.

I haven’t seen any discussion on further well plans for Baúna. The little provided geologic topology doesn’t show any nearby structures of interest.

The known reservoirs seem to be well covered in terms of well drainage and it may be a case of just producing the wells through their economic life. This should require very little capex. In my production model I estimate the field is roughly economic until ~2030 using an arbitrary 5 kbd oil cut off level. Karoon’s reserves are based upon Baúna running through 2032 so there is some error in the tail of my model here44. This is especially so given the solid unit economics of the field. When you can make a 20%-30% return by simply maintaining the status quo, it's logical to do so. This is not the time to do anything fancy with the asset.

More clarity on potential future plans would be nice to see. The FPSO could in theory become a donor to Neon/Goia (or another nearby discovery) in the early 2030’s. These ships can last a very long time, especially with a little dry dock between fields.

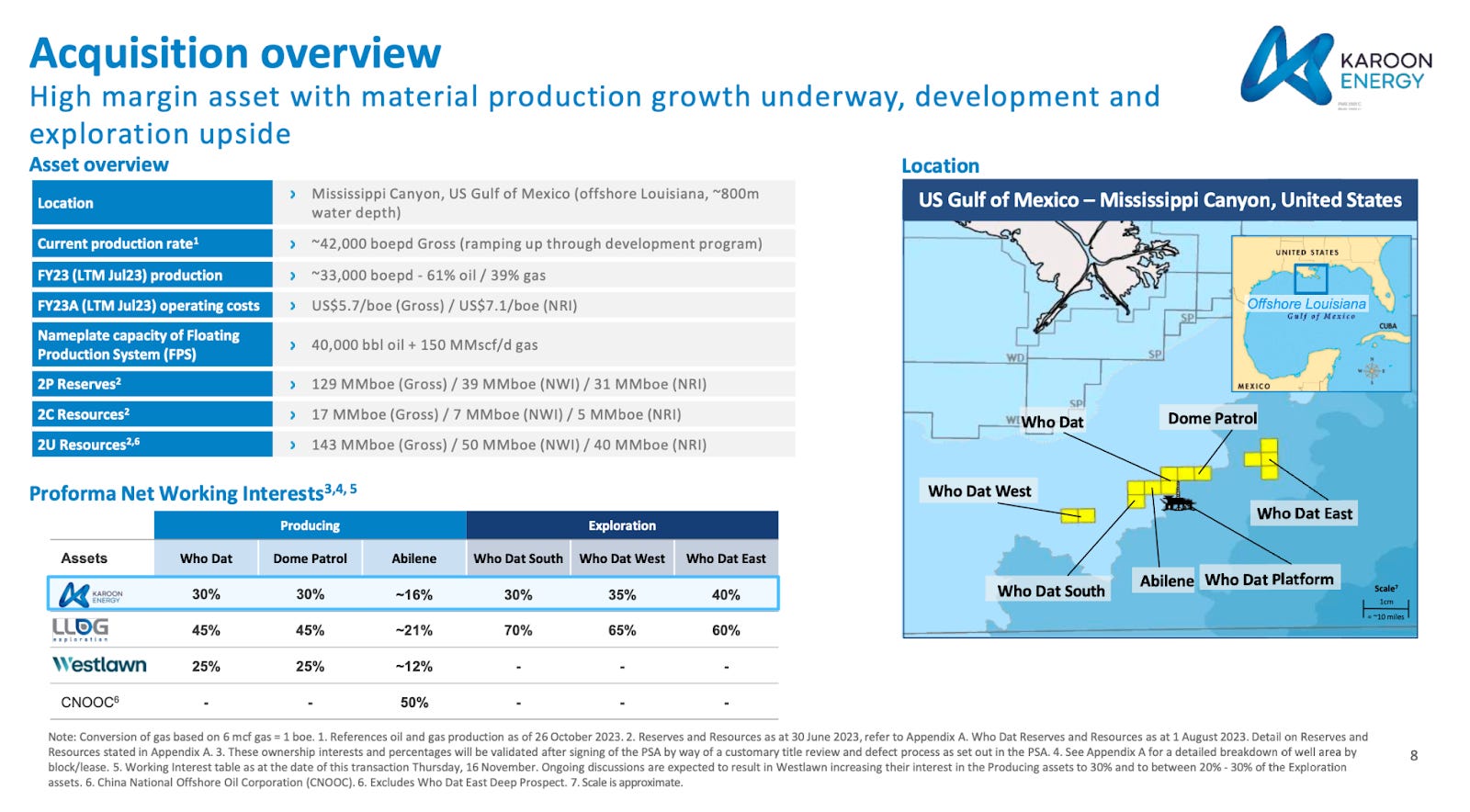

Who Dat

I will keep my Who Dat discussion a little briefer. There is also a lot less data available on Who Dat and the asset is quite similar to Baúna.

The important points to note are:

The field is operated by LLOG in the Gulf of Mexico (GOM) and Karoon owns a minority share of the field (~30%). meaning they are not in control of decisions but merely have 30% influence45.

The field is much more gassy. Baúna is a purely oil operation (the produced gas is re-injected), here we have available gas and oil export pipelines (reducing transport costs too). The value of Gas in the GOM is very low, export prices to Henry Hub are around $2/mmbtu. Who Dat production is quoted in terms of boepd, however this is on an energy content equivalence which is approximately 6:1. A better ratio for an economic equivalence would be around 35. Gas is fundamentally very cheap and can be nearly completely discounted from the production figures.

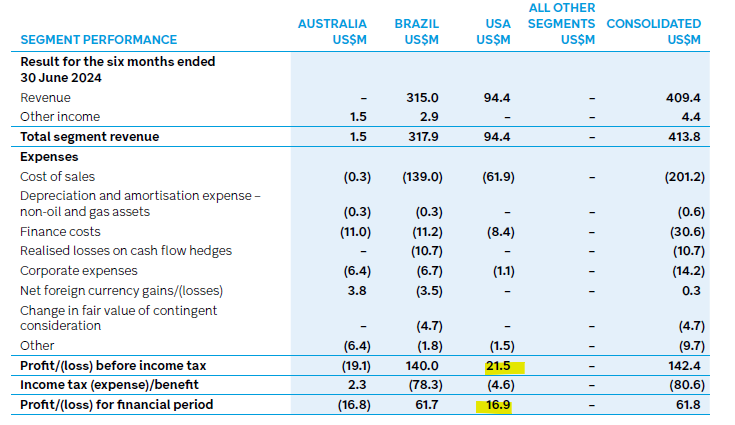

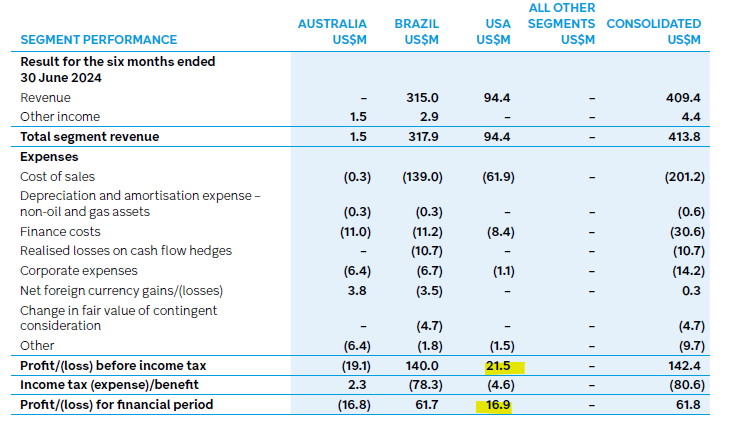

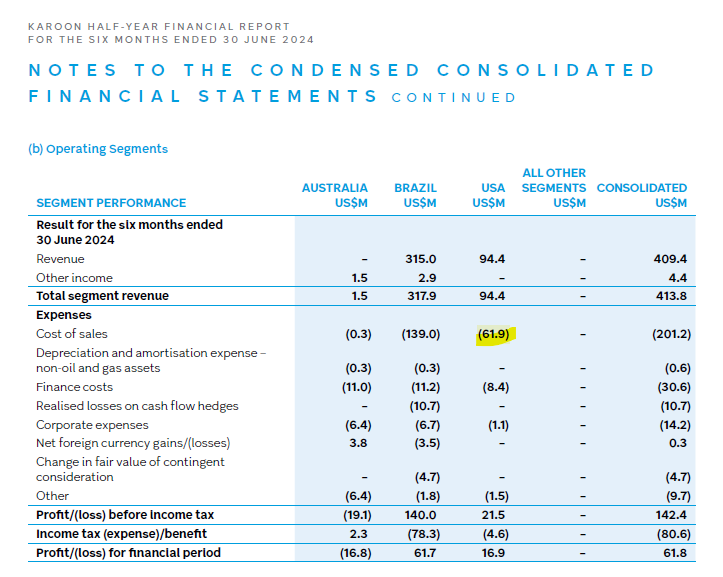

Who Dat makes a lot less money. CY24H1 net profit was just US$15M following spending $720M on the asset. Costs are not as transparent due to limited history of disclosures on the asset.

Some reservoirs hold condensate, which is a highly valuable liquid form chemically similar to gas. Condensate is a very clean hydrocarbon which is a precursor to jet fuel or otherwise used in blending. Its value is approximately the same as oil per bbl.

The host unit has pipelines directly into other fixed assets, so there is no offtake need46.

The field is much more scattered and complex in terms of reservoirs, field size and potential. However the reservoir properties and geology are very similar.

Acquisition

As previously discussed, Who Dat was purchased in late 2023 for US$720M. Adding an additional material asset was a core management goal for the reporting period, that plus the decline of Baúna creates pressure to purchase new assets to survive. Karoon also had significant net cash at the time (ca US$152M), burning a hole in their pockets.

The Acquisition of Who Dat in light of the 2024 operational performance and figures vs the initially disclosed presentation is nothing short of disastrous.

In case the above statement is in doubt:

The capital losses in Karoon market cap since the acquisition have exceeded the cost of the asset.

Production Guidance was revised down 3 times in 2024, including in the very first quarterly (March 2024), around 100 days after investment.

Who Dat contributed US$16.9M of net profit for 1H24 on US$94.4M of Revenue. This is ca 2% return in 6 months on a “High Margin Production” Asset. (to be fair, in my theoretical longer term case this should be closer to US$39M).

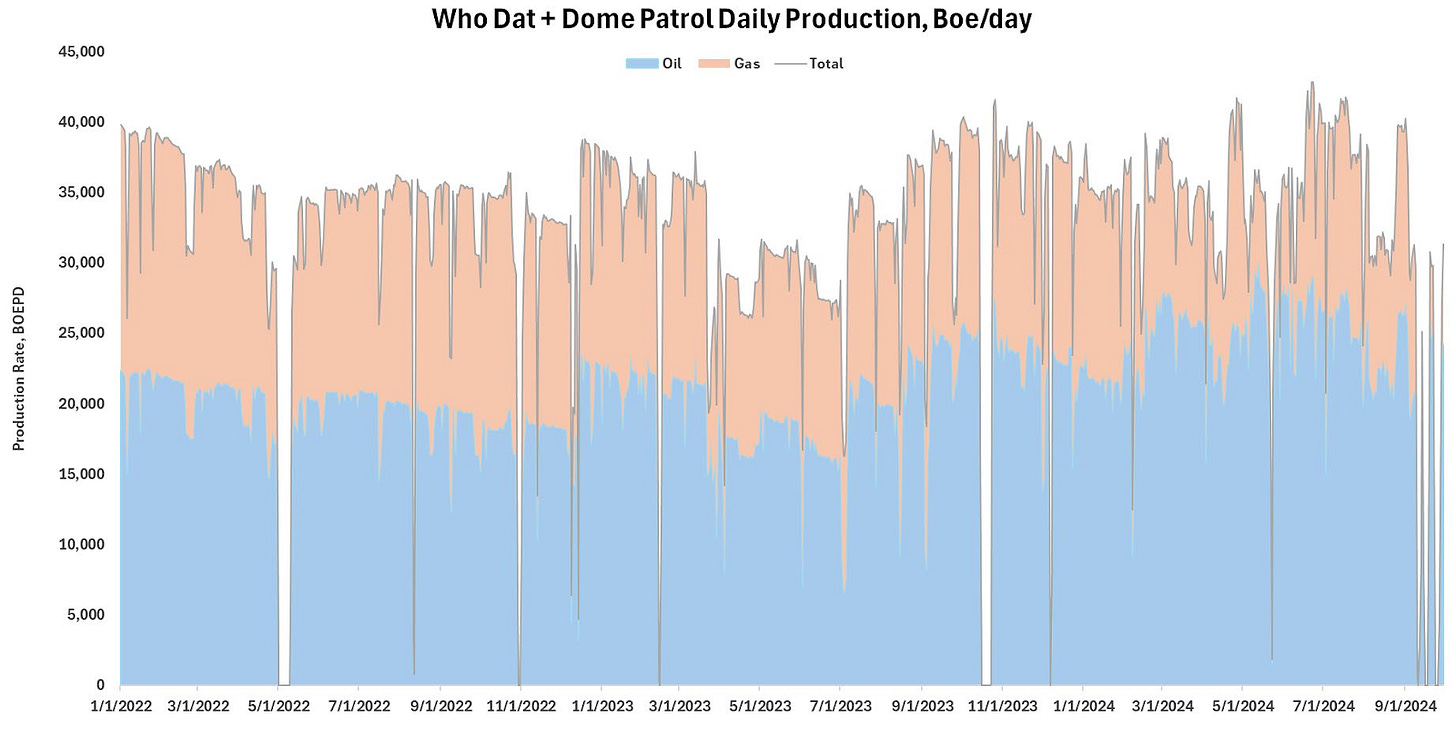

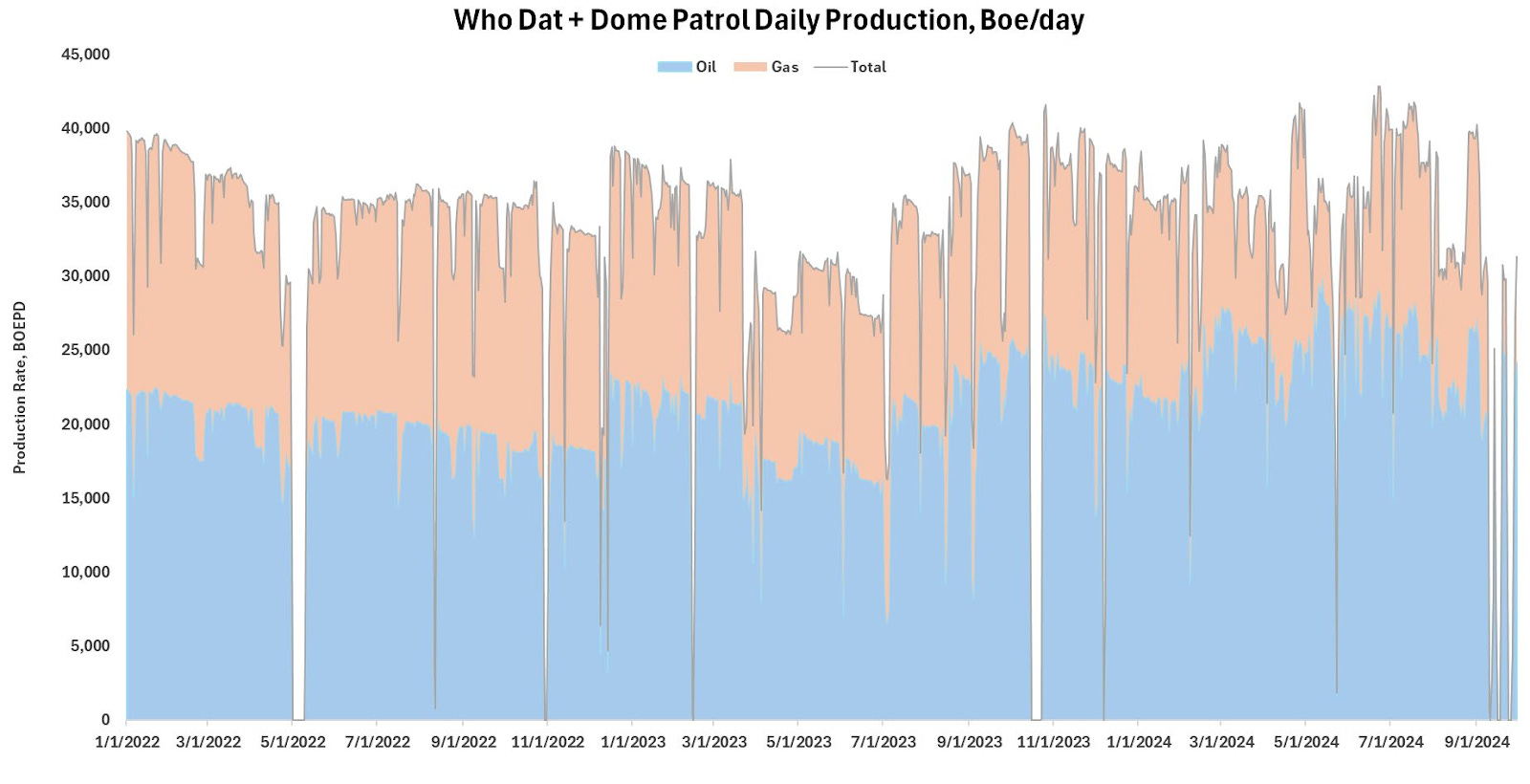

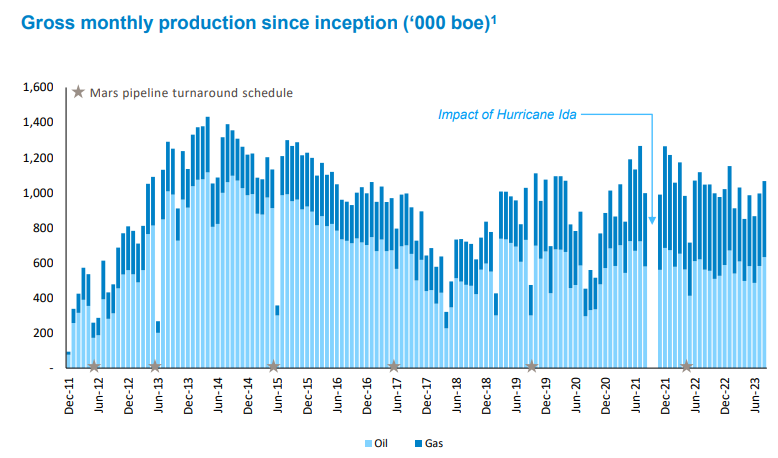

KAR 1H 2024 Results pg 22 (2024-08-28) Presentation discussed a 42 kboe/d as the current gross production rate, however this instantaneous rate has hardly ever been achieved at the asset. This is best seen with a chart released in late 2024 (almost 12 months following the acquisition).

The first quarterly had Who Dat gross production of 34,962 boe/d, 16% less than communicated.

Who Dat Gross Production (boed) - Karoon Slide - KAR Field Trip (2024-10-31) Presentation is highly focused on adding reserves, but so much of these reserves are gas they have gone from a near fully oil based book to a very gassy book.

Lets quickly summarise some of the key comments from the initial Investor Presentation on Who Dat:

“Mid teens cash flow per share accretion and EPS accretive”

“Low cost barrels to deliver long term cash operating margin of 67%

“Expected to be earnings and free cash flow per share accretive from CY24”

There’s a very strong case to be made that Karoon would be a much stronger company currently if they never purchased Who Dat. The company would have spend US$800m less, exceeding its current market cap.

Geology

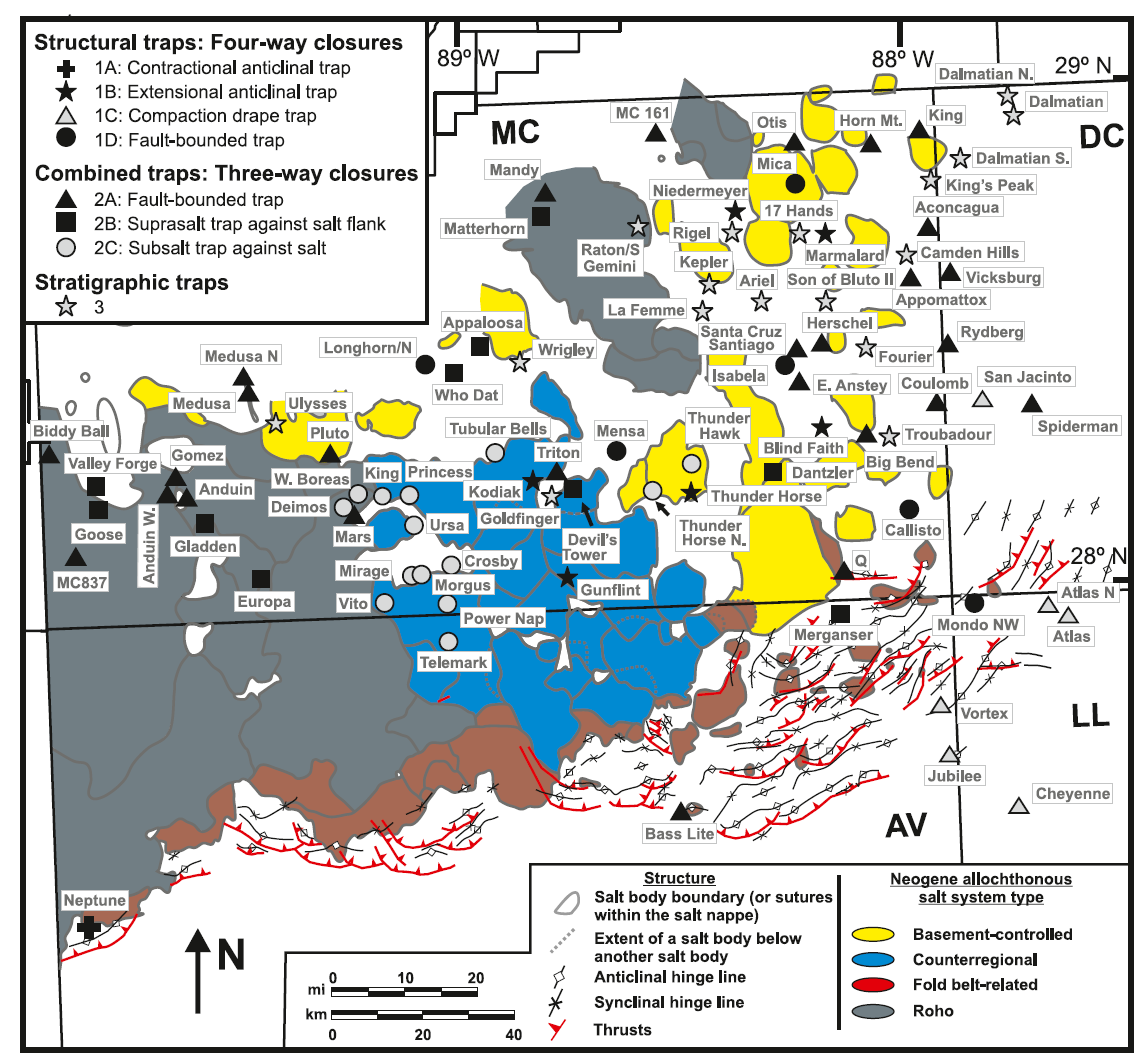

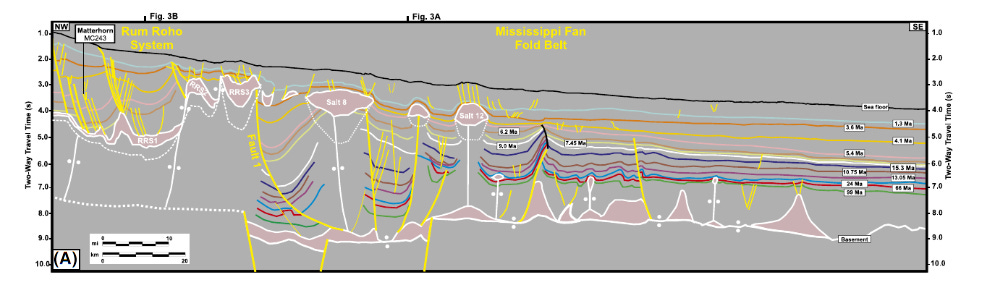

There is little discussion by Karoon about the Who Dat Geology. The wider Mississippi Canyon Block in the GOM is large and well studied. I’m personally unfamiliar with the area, however it looks well picked over and highly complex.

The Mississippi Canyon (MC) block sits at the mouth of the Mississippi and is defined by sedimentary deposition down the continental slope for millions of years, with many channels, faults, traps and salt domes47.

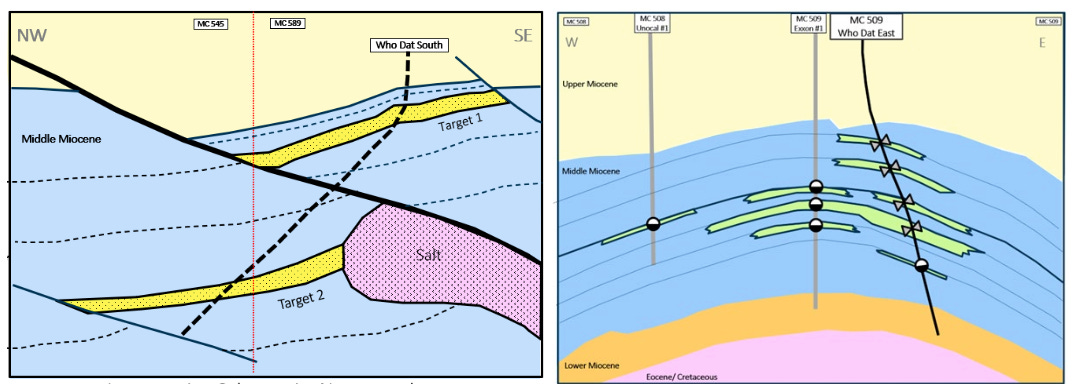

Below is a nearby seismic cross section with interpreted faults, the multiple layers of sand and salt domes, roughly reflecting the type of geology likely at Who Dat48.

The Who Dat field is characterised by many (11+) stacked Pliocene and Upper Miocene reservoir sands situated around a salt dome, at around 10,000-18000 ft in . Disclosures note the reservoirs are ‘high quality’ turbidites, with high porosity and permeability. This is generalised, but very similar to what exists at Baúna. Reservoirs are all different pressures and hydrocarbon types.

This field geology is best seen in the exploration communications, displayed below:

Field Development & Wells

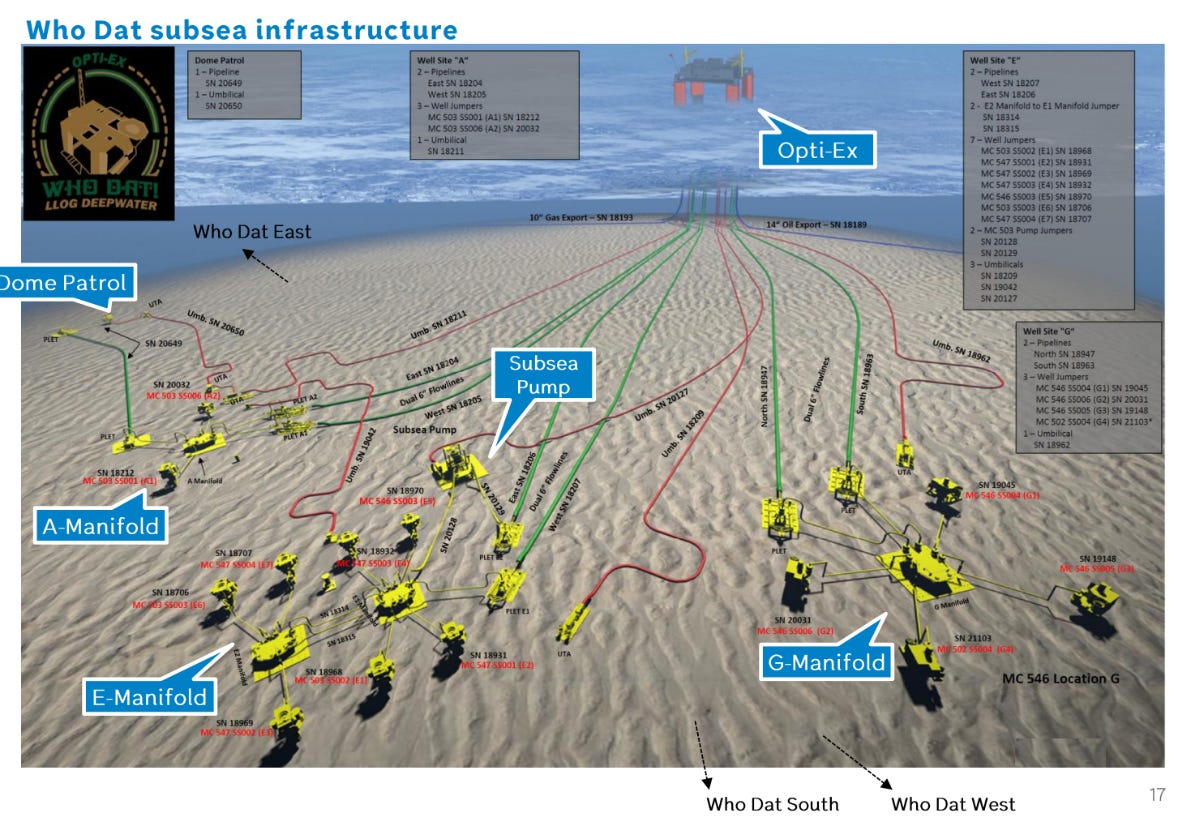

The field was developed by LLOG around an Owned “FPU” called “Opti-EX” produced by Exmar in 2010, with capacity of 40 MBOPD49 and 150 MMSCFD. The FPU is tied into a 10” gas export line and a 14” Oil export line.

Each manifold has dual 6” flowlines, which are approx 5km in length. The Dome Patrol well is a step out, on its own ~5km flowline to the A-Manifold.

The Production system is likely completely from TechnipFMC.

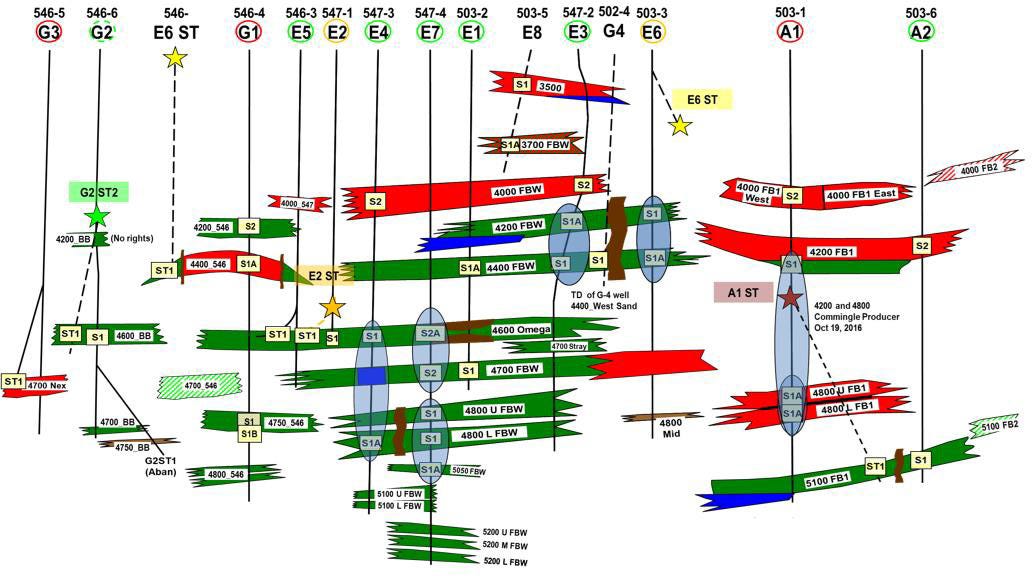

Wells

I have collated the well data from disclosures. Data quality is lacking due to the nature of the scattered sources I have collected these from.

The field is often talked about as having 14 or 15 wells with one of them not producing50. There are a couple new drill wells G2 and G4. Another had an ESP installation.

There are 3 subsea manifolds51 (A,E,G) that the wells flow to.

Manifold E is across the middle of the field, is the prolific and most valuable.

G-Manifold is out west and accesses Abilene, a large gas reservoir. This manifold is the most gassy.

A-Template is North. Dome Patrol is far out east with a subsea pump into a slot of the A-Manifold.

Production

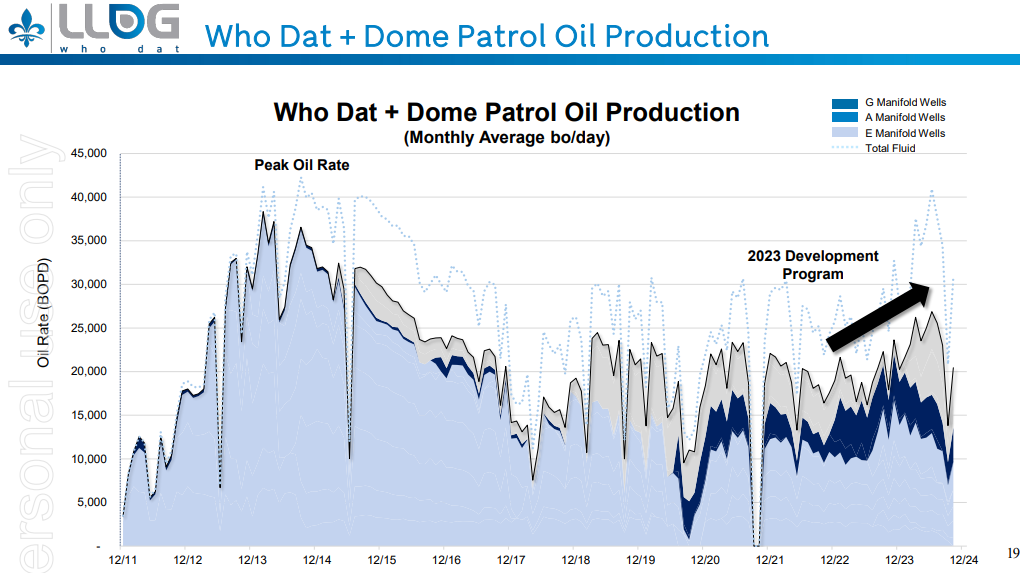

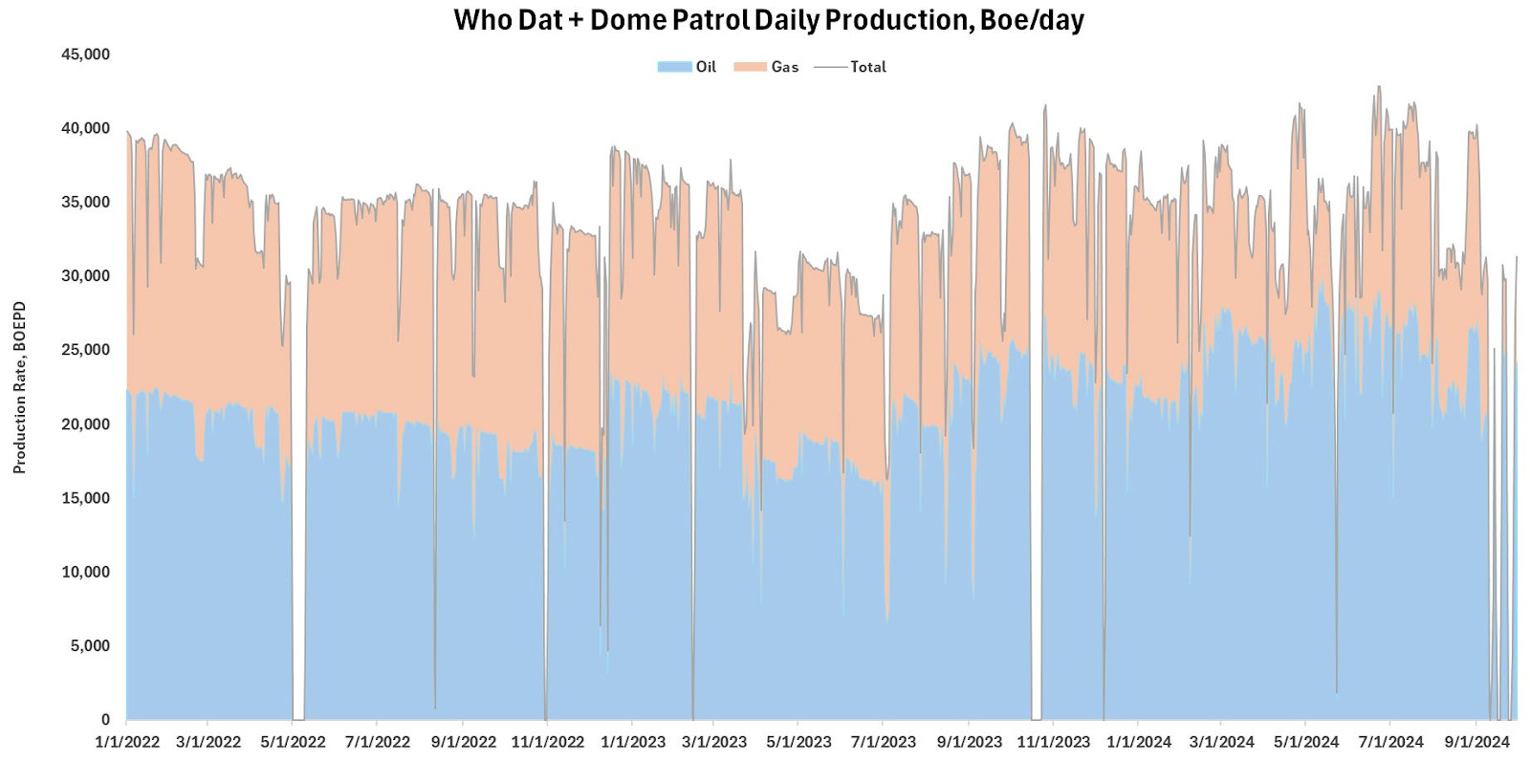

We have a few charts on the field's production, note one is Oil only and others are BOEPD. Note the large gas cut (%) of the BOEPD production rate. This large gas component makes the asset production figures almost twice what the core value really is.

Modelling the asset at around 20 kbd oil is reasonable.

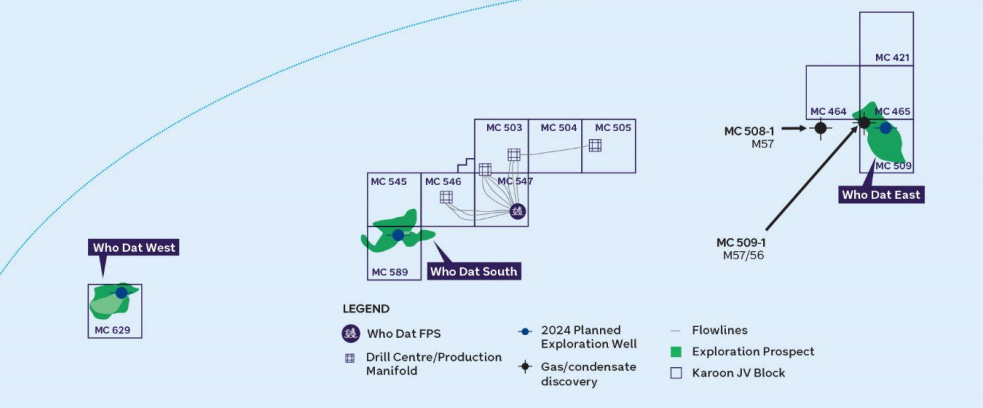

Near Field Exploration Wells

The Who Data licence has a 3 well active exploration campaign ongoing. LLOG have active rigs in the GOM which are shared across leases.

LLOG seems like a reasonable developer with good turn around times from exploration to production, just they are taking Karoon in a whole new Capex heavy direction. The three drill wells are all within tieback distance to Who Dat (just) and are follows:

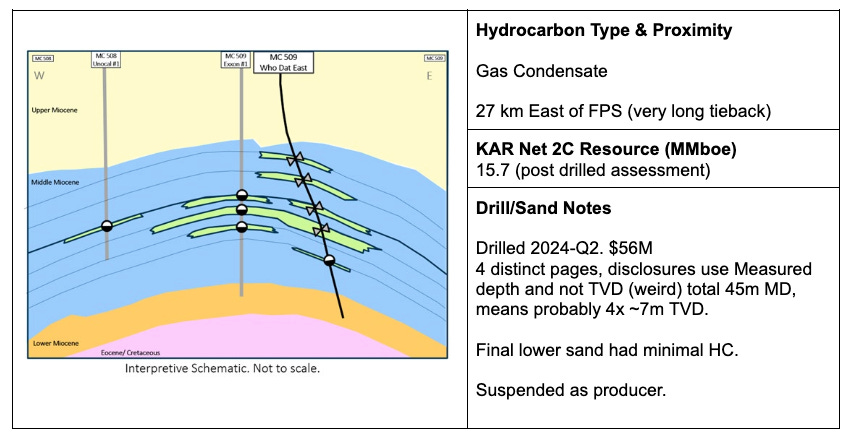

WDE - Who Dat East

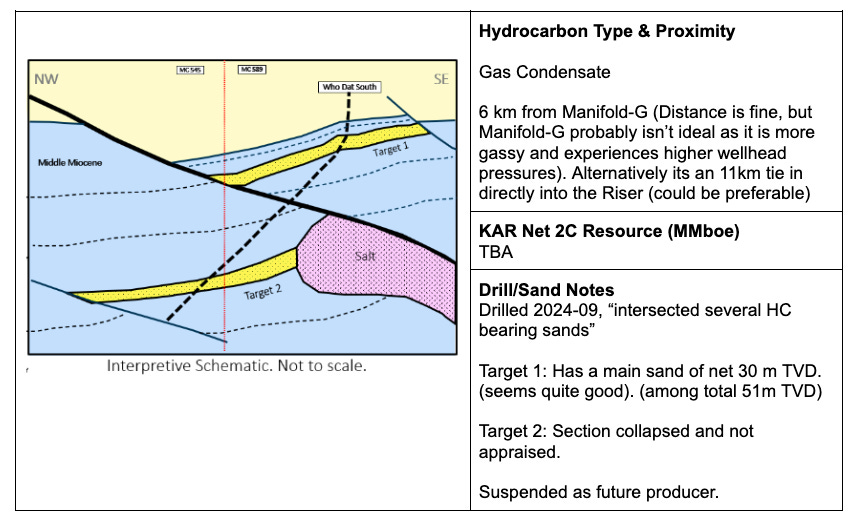

WDS - Who Dat South

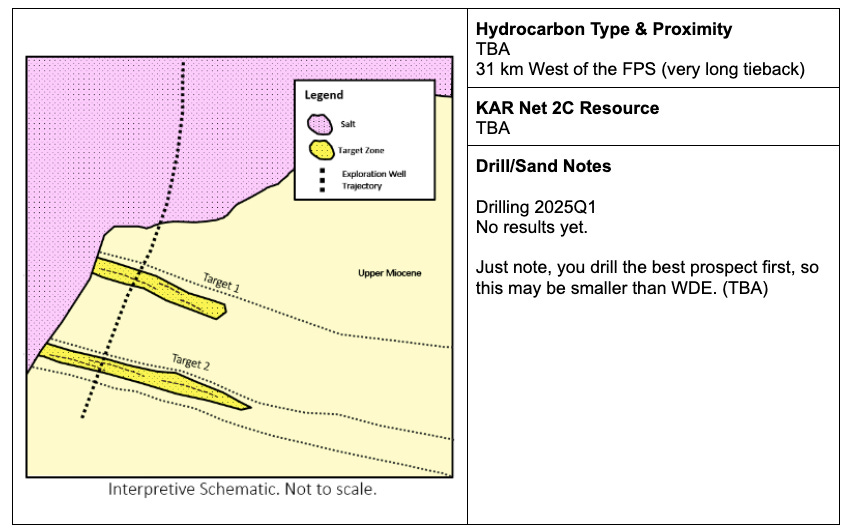

WDW - Who Dat West

Downtime Events

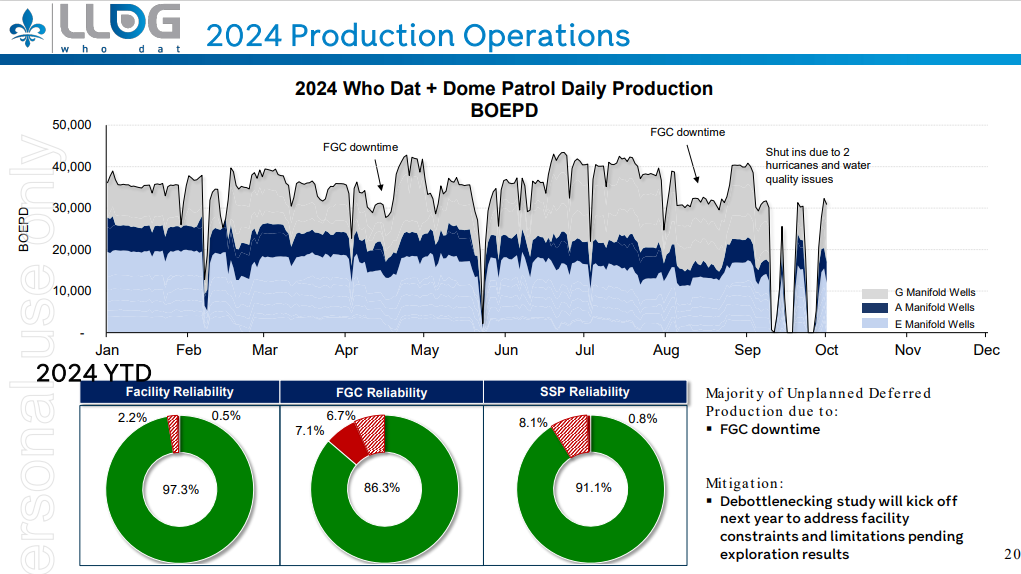

The Who Dat downtime has been mostly linked to planned shutdowns and preventive downtime due to hurricanes. Following the new wells at the G-Manifold, gas production levels were creating higher wellhead pressures, limiting oil production. Wells were cut back to prioritise oil cuts during a time of low gas prices.

2024-Q1 High Back pressure in G-Manifold, cut back high rate gas wells.

2024-11 (10-14d) Planned Maintenance Shutdown turned into 18D

2024-09-10 Shutdown due to Hurricane Francine. 3d shut in. Reopened on 12th

2024-09-25 Shutdown due to Hurricane Helene. 3d shut in. Reopened on 27th

Taxes & Royalties

The royalty is 12.5%, US Corporate tax is 21%. Assume no state charges as the sales transaction occurs offshore and not within a state boundary.

Costs

There is a challenge in the Who Dat data, such that not only do we not have a full annual report available for the asset, the Sales are communicated in NRI which is already adjusted for royalties.

However when we get into the 1H24 Financials, the Cost of Sales number is dramatically high and theres no visibility on why.

In the Supplemental bond issue docs the costs were communicated at $7.88/boe for 12 months, but that only accounts for -$13.4M of the 61.9M.

The depreciation step up from TY23 to 1H24 was -60.8M to -82.3M, so I can assume an additional $21.5M of halfy depreciation at WhoDat

I am in the dark on whats going on here and I hope this largely consists of some sort of once off charge. Point is, we know the NPAT for the asset is extremely low: $16.9M.

Where to from here for Who Dat?

This asset is a poor fit within the organisation due to its capital needs and current ROE vs the companies profile before this asset. If a reasonable offer was made on purchasing KAR’s Who Dat stake it should be strongly considered (despite the sunken costs).

Mitigate CAPEX. Stop spending, it has destroyed KAR’s free cash flow which was the one thing going for the company.

Further discussion on discretion of the full CY2024 results. More visiblity in Cost of Sales is needed.

WDE and WDS drill wells seem reasonable. Complete these and tie them into the asset.

STOP further development of this asset and let the cashflow come through. (It seems ridiculus, the Net Profit is about the size of their corporate costs).

Management

There has been a lot of ink spilled in the media over the management situation. There is a large overspending and over commitment issue. The company has quickly jumped into being a Producer of two distinct assets and is frankly doing too much and has lost focus on the core responsibility of managing the company equity appropriately. Karoon is now a very different organisation, away from their core goals and to a point where the company's free cashflow has now evaporated.

Spending

The company has quickly turned from looking like Baúna was close to fully paid down and moving to a pure liquidation focus with strong FCF, yet now, the company would be close to FCF neutral as Who Dat exploration has drained excess cash. This spending in itself is not problematic52, but the circumstances and timing of the spending53.

Karoon undermined their own principle from their 2021 Strategic Direction of “In Control of our Destiny”54, but also their original direction to be Brazil focused. Specifically undermining their strategy of “Brazil M&A”, “Neon Area Development” and “consider complementary strategic oil acquisition opportunities”. Not to mention the other objective of “Operational Excellence”.

Buying a field nowhere near their existing operation is not complementary, especially where they were going down the pathway of having an Integrated Operational Area55 in the Santos Basin. It has in fact stretched them too far.

Surely they will take a victory lap soon about how successful their 2021 strategy has been in their 2025 refresh. I will be happy to be corrected.

The diversification away from being 100% in Brazil seems reasonable. There is no mention of any expansion ability at Baúna, and some activity at Neon with modest and risky potential. Perhaps it's unwritten that there is not a lot of confidence in Neon/Goia, whilst production rates (and earnings) are dropping.

This is all easy to say now (late 2024), following Who Dat for a year, this would have been much harder to see on announcement of the Acquisition.

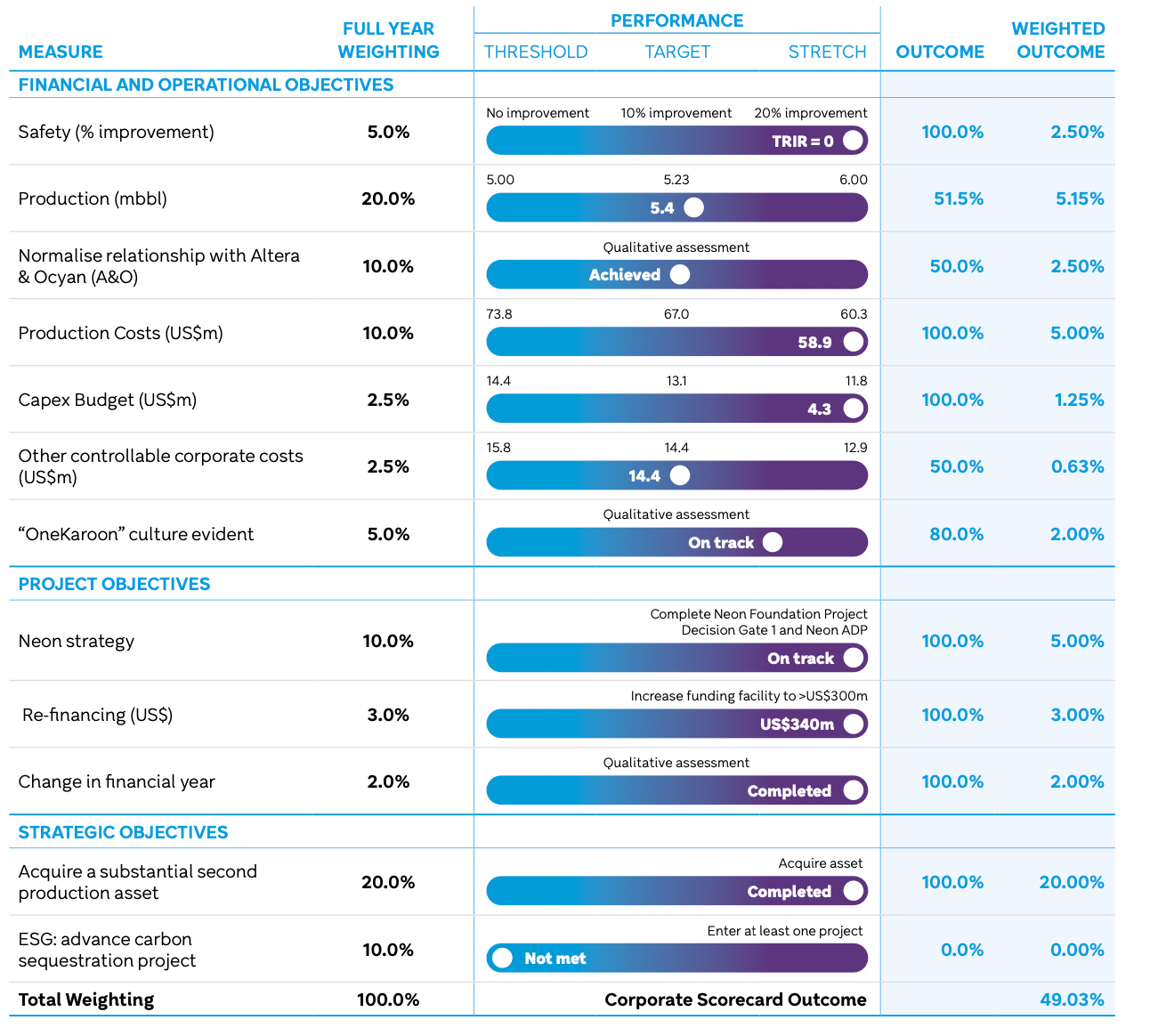

Previous Management Scorecards

Below is the score card for TY2356 which the management's performance bonus is based upon. This is the most recent one as of late 2024.

One can quickly see the Safety performance of the company is weighted nearly identically to the “Project Objective” of changing the financial calendar for the company. This is beyond ridiculous.

(In an earlier score card there was no weighting for safety).

What is perhaps worse is that the Strategic objective of “acquiring a substantial second production asset” is weighted 8x times more important to safety. The FPSO may have sunk, yet this wouldn’t affect management's bonus incentive more than purchasing Who Dat. Yes I am being ridiculous, but this is a logical outcome of the management scorecard.

I get a sense of ‘no fatality’ meaning bonuses from reading the TY23 Karoon remuneration report. This is probably written by people sitting in a fancy office on Southbank in Melbourne57, whereas the real risk is outsourced.

Conclusion & Current Opportunity

Whilst the above commentary has not been rosy, the equity market has similarly provided its own fairly damning assessment. Karoon is currently priced on the ASX at $926M. The opportunity in Karoon is in the context of this market pricing.

Strategy Issues

There’s a temptation to go back to the simplicity of a single Brazilian asset and just cashflow the asset. But given the damage to the companies equity valuation, looking forward to Who Dat asset adds a lot to the business. There are probably a lot of positives for Karoon if Who Dat was divested immediately at a fire sale price and Corporate costs were tightened up, this is however shortsighted58.

Who Dat seems to have a lot more life and better risk adjusted upside potential than the Baúna/Neon/Goiá Area. From this deep dive I get the sense that Karoon are struggling to find ways to economically expand in Brazil and therefore have grown into the GOM instead. 2 of the drill wells seem reasonable and will add volumes and $ to the field immediately. The partner also seems reasonable.

The strategy has deviated heavily, the downtime at both assets has been inexcusable, however this is a reflection of the past and current state.

Valuation Issues/Opportunity

The ‘upside’ is that the equity has been so severely punished that it is priced at a point where the entirety of the Who Dat acquisition has been eliminated from the Market Cap and more.

Prior to the Raising, the SP was $2.40 with 567M SOI for $1.36B Market cap.

Currently at $1.30, the Market cap is ~$1.0B59, ($1.20 was $0.92B, $1.40 is $1.07B)

This is approximately $300M below the current market pricing, with Who Dat vs without.

This level of equity valuation is likely sufficient to value Baúna alone (assuming we get good uptimes). Applying a multiple on a declining asset is fraught with danger, but the yearly free cash flow from Baúna should be at least AU$300M/year for the near future.

This implies Who Dat is never going to be cash flow positive, or is effectively not included in the current market price of Karoon Equity. This is of course ridiculous.

Who Dat is an 8 kboed asset (Net NRI) which could be liquidated. There are 2 nearfield drill wells which have had much of the cost and technical risk sunk.

When your asset is priced at presumably ~50 cents on the dollar, why would you focus on drill wells, field development at “mid teens IRR%”, when you can get a ~100% return in the short term by performing buybacks and getting to a share price that existed a few months ago.

The market is not rewarding any of the development capex, this money has been taken from Karoon’s balance sheet and essentially lit on fire, instead of simply leaving it alone or returning it to its owners who are better placed to look after it.

If the above isn’t clear enough for Karoon Management, I have another big suggestion: Stop Issuing new equity.

Grow your business without raising equity at every stage. Karoon has a market cap of A$1B yet has Contributed Equity is US$1.21B. This is close to nearly every second dollar having been lit on fire.

Following all of the above, once the market cap is a bit more healthy, management should consider upping the dividend. Continue the liquidation of the assets into cash flow for equity holders.

Become known on the ASX for having a ridiculously high dividend.

See if the dividend can be held at a A$0.20 to $0.30 fully franked dividend annually for a few years. See where the price and yield settles, presumably its 10-15%. ASX investors will be all over this ASX investors have a strong preference for dividends and this domain is dominated by Coal Players, which many are turned off by and will indiscriminately avoid under any circumstance.

Very few companies have this opportunity. Don’t let it pass by pissing the cash into holes under the seabed. Put it into the hands of your shareholders who may then hate you less next AGM and not try and get you kicked out.

Summary

I would theorise most of the downside risk is already in place at this point in time, and the upside considerably outweighs the downsides.

The equity has been deservedly punished, but there has also been a situation of a lot of bad luck too. I am optimistic that 2025 is much less operationally challenging for KAR, that earnings will reflect this.

The company needs to stop empire building, tighten up the spending and focus on the common equity holding.

Editor’s Note

My background is in Completion Engineering, Subsea Engineering and self learned many aspects of finance and economic assessment. I am interested in Karoon due to:

They are a local Aussie company (its a little parochial).

Their assets are analogs to what I’m fairly familiar with.

They are small enough to be awfully specific when they give details on field, so I can relate to the wells, reservoir and vessels.

They are fairly hated by the market, liquid and interestingly priced.

Low coverage in this name. I may have some value to add to the finance community, with a more technical subsea lens.

Disclosure

This information is for general knowledge and informational purposes only and does not constitute financial, investment, or other professional advice.

I have a small long position established recently, post the Who Dat acquisition and operational issues.

I have no association with the company other than the equity holding and never talked to a Karoon employee or anyone who has worked on their assets.

No Assistive Technologies were used in the creation of this material. I didn’t even run a grammar check sorry :) .

100% owned and Operator, meaning responsible for the day to day operational needs

~30% owned and non-operator, LLOG is the operator. Minority non-operated is a position where you can strategically influence but do not control the field.

Having multiple productive fields in a close area is a strategic positive I will come back to later.

2021-10-28 ASX Release.

Who Dat!

LLOG has 2 active drillships in their portfolio. Source: ASX Disclosure 2024-10-31 “Karoon Field Trip Presentation”.

The Seadrill West Neptune through 2026-01 (with extension options to end July 2026): https://s203.q4cdn.com/237508583/files/SDRL-Fleet-Status-Report.pdf

The Noble Valiant through 2025Q1. Day rate of $470K, plus overheads and other crew https://s201.q4cdn.com/439848451/files/doc_downloads/2024/07/FSR-073124.pdf

Rig operational expenses for 2 Drillships likely close to $1.5M/day to the operators, plus the well hardware.

Drill wells are discussed later.

I am hesitant to refer to the market's price action as a reflection of actual performance, but in this circumstance it is highly notable considering the very large drop in the price of Karoon’s equity price (KAR.AX / ASX:KAR).

Namely Samuel Terry Asset Management & Sandon Capital.

Take a look at US centric names like Diamondback Investor Relations presentation packs and there is more discussion on capital framework and capital returns than the underlying assets themselves.

$2.09 on 2023-11-15 to $1.175 on 2024-12-18, net a 4.5c dividend. =(2.09-1.175-0.045)/2.09

$2.67 on 2023-10-19 to $1.175 on 2024-12-18, net a 4.5c dividend. =(2.67-1.175-0.045)/2.67

This Article took a little longer than expected to complete. The price has girated around $1.18-$1.40 mark during writing/publishing.

Echidna-1 (discovery well) in 2015, Neon-1 and Neon-2 in early 2023.

Note current Baúna reserves are ~40 MMbbl Proved (1P) and ~55 MMbbl Proved and Probable (2P).

Kangaroo-1 (discovery well) in 2013, Kangaroo-2 in 2014.

Addressed more specifically shortly.

These are likely US$100M per well to develop. FPSO costs I have not dug deeply into, but these are far from commodity products. $XOM’s Guyana is easily $2-3B per FPU and they have a large order and set designs. Best scenario is a refurb of existing FPSO.

Ballpark AU$2B-3B?

ASX 2024-10-28 Brazil Field Trip.

Baúna was purchased pre-Patola, however the Patola wells had already been appraised and were ready to go.

If it hasn’t already been so.

Goldman Sachs has Neon/Goia capex at ~$2B over 2026/2027 believing KAR will go ahead with it in its basecase. Market is pricing Karoon Market Cap of ~AU$1B, this leaves no room for any value assigned to the development.

This is shallow for subsea.

~34° API, light sweet crude. Patola was 38° API (even higher quality).

FPSO is Floating, Production, Storage & Offtake. Cidade de Itajaí is a converted Aframax. The ship always stays in the same place and is permanently moored to the sea bed.

TVD = True Vertical Depth. m=Metres, SS=Subsurface.

You wouldn’t put your worst sands into the disclosure, I presume these are on par with the best in the field.

This section was added in late January 2025. I want to preserve the original integrity of the article (as its fundamentally a directional bet), but this sand quality is a critical input into the quality of the asset.

SPS-56, SPS-88, BAN-1.

BAN1- and PRA-1.

In 2011 the Gryphon Alpha FPSO in the UK lost a few mooring lines in a bad storm and caused US$1.8B damage. A field economics killer.

Where the original operator may see the asset as non-core and cut capex, or the new operator doesn’t maintain previous operators' processes.

See how the comms on this issue are strange?

There is a small interest and discount rate component which affects the final amount slightly.

Which I do not pretend to understand.

The oilfield is famous for pointlessly complex tax rates, Brazil seems to tick this box.

This range may seem strange as it includes 100%, but it's more a matter of how many trips/attempts are made and how many days are burned re-trying the same operation. It's common for a GLV replacement to work first or second time. It's also common that more technical problems are found during the operation and the lack of information and equipment limitations don’t allow any further pathways to success. In that case it's a very expensive tubing pull operation with a rig at a later date. KAR would be highly unlikely to bring a rig over SPS-88 for only 2kbd.

Macro is not the focus here. Despite the situation, I do think US$70/bbl is historically low inflation adjusted.

The tail in my model is far out and unimportant.

Most decisions would require a majority vote within the Joint Venture (JV).

Therefore it is abbreviated as FPU (Floating Production Unit), or FPS (Floating Production System). No need for Offtake (O).

Following images are all from “Regional structural setting and evolution of the Mississippi Canyon, Atwater Valley, western Lloyd Ridge, and western DeSoto Canyon protraction areas, northern deep-water Gulf of Mexico” https://www.researchgate.net/publication/318082257

I will update this if any Who Dat geologic data is released. I can not find any online.

I’ve seen references to both 40 kbod and 60 kbod.

Presumably long term shut in, not known which one.

Or “Template” which I may use interchangeably.

That is, the spending on new potential wells is productive, but it seems like LLOG’s cost of capital is lower than that of KAR’s.

Both installations have experienced downtime events, oil has been weak, KAR dropped to below $1.20 and instead of taking advantage of this they spend the money exploring.

2021-10-28 ASX Release, page 13

Integrated Operations are common in the oil space. Having multiple partially dependent facilities in the same location provides expected and unexpected synergies. A single operational hub and shared transportation facilities and contracts is of course obvious, what's less obvious is the flexibility that is introduced when things change. The oilfield is filled with change and uncertainty, especially in mid-late life fields. Having lots of extra assets in the same area enables more create options (Vessel sharing, flowline/processing sharing, common infrastructure, re-prioritisation of vessel resources).

CY23H2 “Transition year”. Enables the move from a July year start to a Jan year start for CY24

Also begs the question, why is there even an office in Melbourne? Get to site guys.

But also probably an excellent outcome. Baúna can provide an idealised A$0.25/sh cashflow in a half, cautiously extrapolated to ~$0.45 in a year. The Market is pricing Karoon at around 3x Baúna annual earnings.

$1.20-$1.30 per share, 770M SOI. Late Dec 2024.